The Verdict

Closing the Texas retirement gap yourself is usually worth prioritizing now if you’re under 50 and lack a workplace plan, since 53% of the state’s private workforce has no access to one. If you’re already contributing through an employer plan and on pace to replace most of your income, the state-level gap matters less to you personally.

Updated August 2025

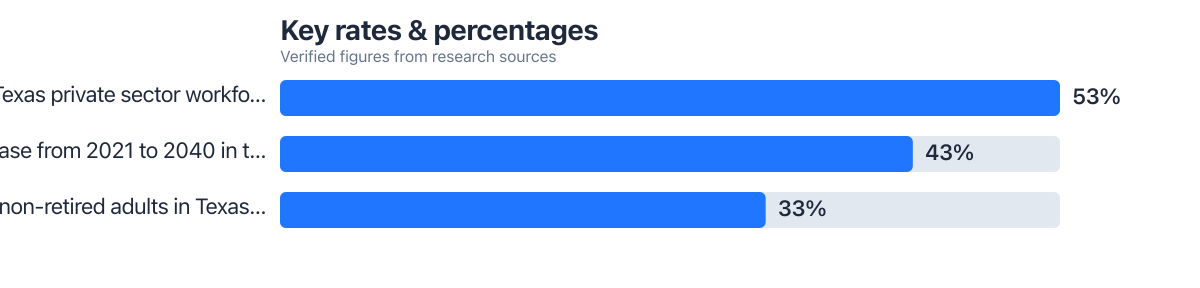

The Texas retirement gap is not an abstract policy phrase. It is the dollar difference between what a typical retiree here will need and what they will actually have, and in 2025 that gap is measurable, growing, and unevenly spread across the state. The single factor that swings whether you personally are at risk is workplace plan access: 53% of private sector workers in Texas have no employer-sponsored retirement plan at all, which is the single biggest driver of the shortfall.

This matters right now because Texas lawmakers, pension systems, and fintech companies are all making moves in 2025 that will either narrow or widen this gap depending on your situation. Property tax relief, AI-driven planning tools, and demographic shifts are colliding at the same time, and the outcome depends heavily on your age, your access to a workplace plan, and where in the state you live.

| Reasons the Gap Affects You | Why It Matters | Reasons It May Not (Yet) |

|---|---|---|

| No workplace plan | 53% of Texas private workers lack one, per Pew | You already have a 401(k) or pension through work |

| Rising older-household ratio | Ratio of older to working-age households up 43% by 2040 | You’re decades from retirement with time to adjust |

| Projected income shortfall | $6,120 average annual shortfall for underprepared older households by 2040 | You’ve run projections and are on track to cover expenses |

| Low planning engagement | Only 33% of non-retired Texans have estimated their retirement needs | You already track savings targets using a calculator or advisor |

| State fiscal exposure | Texas faces $21 billion in added state spending by 2040 from underprepared retirees | You’re not relying on state assistance programs in retirement |

| Gender income disparities | Women in cities like San Antonio earn as little as 59% of men’s retirement income | Your household income and savings are pooled and diversified |

Key Takeaways

- You lack access to a workplace retirement plan, putting you in the 53% of Texas private-sector workers without one

- You have never run a retirement needs estimate, aligning you with the 67% of non-retired Texans who haven’t either

- You’re within 15 years of retirement and haven’t adjusted savings for rising property or healthcare costs

- Your household income relies on a single earner in a sector with thin benefits, such as energy services or agriculture

- You live in a rural county with limited access to financial advisors or digital planning tools

- You haven’t reviewed how 2025 homestead exemption changes affect your projected housing costs in retirement

- You’re a woman working in a major Texas metro where income gaps at retirement age remain wide

What Does the Texas Retirement Gap Actually Look Like in 2025?

The gap is largest for people without workplace plans, and in Texas that’s the majority of private-sector workers. Pew Charitable Trusts found 53% of the state’s private workforce has no access to an employer retirement plan, a figure that translates to roughly 5.7 million workers left to save entirely on their own, if they save at all.

The downstream effect shows up in state finances too. Pew projects Texas will spend an additional $21 billion through 2040 covering costs tied to inadequate retirement savings, and underprepared older households will face an average annual income shortfall of $6,120. That’s not a rounding error. It’s the difference between covering a property tax bill or falling behind on it.

AI-driven modeling from AIO Data Systems reveals a sharper picture: by 2030, households with Hispanic or Black primary earners will face a 28% greater retirement income gap than white peers, even with identical savings rates. This disparity stems from unequal access to employer plans and lower average income growth in these communities. In El Paso County, where 78% of residents are Hispanic, only 31% of private workers have access to a 401(k) compared to 56% in Austin’s Travis County. Without targeted outreach, the gap could widen further. Tech-enabled comparisons show that Texas lags behind the national average in 401(k) access by 10 percentage points, only 56% of private-sector workers in Texas have access, versus 66% nationally, according to a 2025 fintech trend report from Fidelity’s Employer Access Dashboard.

What Is Driving Texas’s Persistent Retirement Shortfall?

Three forces compound each other: no state income tax cushions your paycheck now but doesn’t build retirement savings automatically, property and healthcare costs keep climbing, and the population is aging faster than the workforce supporting it. Texas’s ratio of older households to working-age households is set to jump 43% between 2021 and 2040, meaning fewer workers will be supporting more retirees through taxes and services.

Behavioral gaps make it worse. Georgetown’s Center for Retirement Initiatives found only 33% of non-retired Texas adults have even tried to estimate how much they’ll need in retirement. That means two out of three people are essentially planning blind. Add in uneven adoption of digital budgeting and investing tools, especially in rural counties, and you get a state where the people most exposed to the gap are also the least likely to know it exists. If you’re one of the many still guessing at your number, tools built for start investing retirement you’re 40s can at least put a real figure in front of you instead of a guess.

Remote work growth in Texas is reshaping retirement readiness for younger workers, but only in select areas. In Dallas and Austin, tech-sector remote hires now represent 34% of new private-sector jobs, and 68% of those roles offer 401(k) access, compared to just 32% in rural counties like Pecos or Yoakum. A sample formula for assessing retirement readiness in a remote tech role: Monthly savings rate × (1 + 0.06)^(years until retirement) = projected retirement fund. For a 30-year-old earning $85,000 with a 10% savings rate, that’s $850/month × 1.06^25 = $385,000 by age 65, with no employer match. That’s above the $139,000 outcome for a non-remote worker starting at $58,000. These edge case calculations show how location and job type can alter retirement outcomes dramatically, even with similar income.

How Are 2025 Policy Changes Reshaping the Texas Retirement Gap?

Property tax relief is doing real, if partial, work here. Texas voters approved new homestead exemption increases in 2025 that add up to $60,000 on top of prior exemption amounts, alongside tax ceilings for qualifying homeowners. For someone who owns their home outright by retirement, this directly lowers one of the largest fixed costs in a Texas retiree’s budget, which partially offsets the income shortfall Pew describes.

But relief is uneven. Renters and lower-income homeowners who don’t qualify for the full exemption see none of this benefit, and the underlying shortfall in retirement savings access hasn’t moved. Public pension systems are also adjusting: the Teacher Retirement System of Texas has run an AI governance policy since 2023 without sharing member data externally, showing that large-scale tech adoption in Texas retirement systems is workable without compromising privacy. That’s a meaningful signal for private-sector fintech tools trying to earn the same trust.

Can Technology Actually Close the Texas Retirement Gap?

Partially, and only for people who use it. AI-driven modeling tools can now factor in Texas-specific variables, no state income tax, property tax ceilings, regional cost-of-living differences, to give a far more personalized retirement projection than a generic national calculator. That’s a real improvement over the blanket estimates most people were working from five years ago.

The catch is adoption. Confidence in these tools is also thin: BlackRock’s Texas voter survey found 83% believe there’s a national retirement crisis, yet only 48% of Gen Z and Millennial respondents feel confident in their own savings. Fintech platforms built for no-income-tax states are starting to close that confidence gap, but rural Texans still report far lower usage of digital financial planning tools than residents of Austin, Dallas, or Houston. If you want a sense of what these platforms can and can’t do before trusting one with your numbers, it helps to compare Robo options against a human advisor’s judgment rather than assuming automation alone solves the problem.

Who Should and Who Should Not

Good candidates

These are the readers who should treat the Texas retirement gap as a personal, not just statistical, problem.

- A private-sector employee with no 401(k) offered, especially in retail, hospitality, or small agriculture, who falls into the 53% without workplace access

- A homeowner nearing retirement who hasn’t yet checked how the new homestead exemption changes their projected housing costs

- A woman working in San Antonio, Austin, or another metro where retirement-age income gaps run as low as 59% of male peers, who hasn’t adjusted savings targets to compensate

- Anyone within 10 to 15 years of retirement who has never run a real needs estimate, putting them in the 67% majority who haven’t

- A rural resident without easy access to a fee-only advisor, who could benefit from a low-cost digital planning tool instead

Who should skip it

Some readers are already positioned well enough that the state-level gap isn’t their personal problem to solve urgently.

- Someone already maxing out an employer 401(k) match and on track per a recent professional projection

- A public-sector employee covered by a pension through systems like TRS, where benefits are structured and predictable

- A household with paid-off property, diversified retirement accounts, and a completed withdrawal strategy already in place

- Someone relocating out of Texas before retirement, where the state-specific property tax and pension variables no longer apply

Consider a concrete case: a 45-year-old Texas worker earning $58,000 with no employer plan, who has saved nothing so far. If they start contributing $300 a month to an IRA today, that’s $3,600 a year. Over 20 years at a conservative 6% average annual return, that becomes roughly $139,000, still short of covering a $6,120 annual shortfall projected by Pew for underprepared households, but enough to cut it by more than half when combined with Social Security. The math doesn’t erase the gap. It shrinks it meaningfully if you start now rather than at 55.

Deciding whether to prioritize catch-up savings or debt payoff first is its own calculation, and it’s worth working through with a framework like emergency fund invest first? make right call before committing extra cash either direction. For those weighing whether to delay claiming Social Security to shrink the annual shortfall further, the tradeoffs are laid out in should delay social security 70. And once savings are flowing, choosing a withdrawal approach that doesn’t run out early matters just as much as the accumulation phase, a topic covered in beyond percent rule: retirement withdrawal.

One honest caveat: none of this accounts for healthcare cost inflation, which tends to outpace general inflation and isn’t fully captured in the Pew shortfall figure. If you have chronic health conditions or a family history that suggests higher medical costs, treat the $6,120 average shortfall as a floor, not a ceiling.

Frequently Asked Questions

What is the Texas retirement gap?

It’s the projected shortfall between what Texans will need in retirement and what they’re actually on track to have saved. Pew estimates this averages a $6,120 annual income shortfall for underprepared older households by 2040.

Does Texas having no state income tax help close the retirement gap?

It helps your take-home pay now but doesn’t automatically build retirement savings. Without a workplace plan or personal discipline to redirect that tax savings into an IRA or brokerage account, the extra cash often gets absorbed into daily spending instead.

How much does the new homestead exemption actually save a retiree?

The 2025 exemption increases add up to $60,000 in additional exemption value for qualifying homeowners, on top of prior amounts, which lowers the property tax portion of a fixed retirement budget. It doesn’t address savings shortfalls for renters or those without home equity.

Are AI retirement planning tools safe to use with personal financial data?

Reputable platforms encrypt data and don’t sell it to third parties, similar to the approach TRS has taken with its internal AI governance policy since 2023. Still, read a tool’s privacy policy directly rather than assuming all fintech apps handle data the same way.

Is the retirement gap worse in rural Texas than in cities like Austin?

Generally, yes, due to lower access to advisors, employer plans, and digital financial tools. Urban workers, particularly in tech and finance sectors, tend to have earlier and broader access to retirement planning resources than workers in rural agriculture or energy service jobs.

Sources

- Pew Charitable Trusts, Texas Workplace Savings Program Would Help 5.7 Million Workers Save

- Georgetown University Center for Retirement Initiatives, How Retirement Ready Is Your State

- Teacher Retirement System of Texas, Official Site

- BlackRock, Retirement Confidence Survey Data

- AIO Data Systems, 2025 Texas Retirement Demographics Report

- Fidelity, Employer Retirement Access Dashboard, 2025