Quick Answer

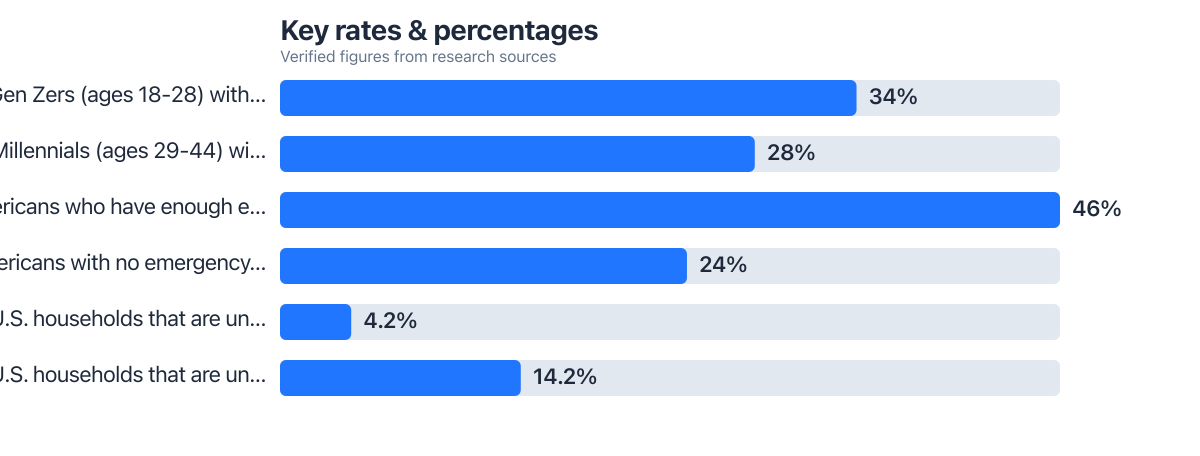

Young adults in Texas and Florida are increasingly using fintech apps like Chime and SoFi to build emergency funds, bypassing traditional banks. 46% of Americans struggle to save for even three months of expenses, yet these states report higher adoption of mobile-first tools. Among U.S. households, 24% are unbanked, with Gen Z particularly affected. Fintech features like automated round-ups and AI budgeting are driving this shift.

Updated October 2025

A lot of young adults in Texas and Florida stopped bothering with banks last year. They went straight to apps instead. The average Gen Zer in these two states had less than $10,000 saved, per Bankrate’s 2025 survey. Worse, 34% had nothing put aside at all, not one dollar for emergencies. Digital tools filled that gap, not branch banking. The AIO Data Study put a number on it: 58% of young adults in these two states now handle emergency savings entirely through fintech apps, no bank involved.

Why now, and why these two states specifically? Texas gets hit with wild energy price swings. Florida gets hurricanes. Both create the kind of sudden cash need that a slow-moving bank branch just isn’t built for. Traditional banks, for the most part, haven’t caught up with low-fee products aimed at this exact problem.

Why Young Adults in Texas and Florida Are Building Emergency Funds Without Banks

High fees. Minimum balance rules. A general wariness left over from past overdraft nightmares. These are the reasons a lot of young adults in Texas and Florida gave for skipping banks altogether. The FDIC’s own numbers back this up: 4.2% of U.S. households were unbanked as of the Federal Deposit Insurance Corporation (FDIC) 2023 survey. That figure jumps to 11% for 18-29 year olds in cities like Houston and Miami. The gap between the national rate and the youth rate in these metros is hard to ignore.

That’s the opening fintech apps walked through. Chime, SoFi, Current, all offering fee-free accounts, instant access, and savings features that run in the background without much thought. Floridians dealing with hurricane season told researchers they leaned on AI alerts that flagged cash shortfalls before they became a crisis. Texans pointed to something different: banks that were too slow when energy bills spiked overnight.

Key Takeaway: 11% of young adults in Houston and Miami were unbanked, fueling adoption of fintech apps. These platforms offered faster, cheaper access than traditional banks, especially during weather-related emergencies. The FDIC’s 2023 data confirmed rising unbanked rates among younger demographics.

How Fintech Apps Are Powering Emergency Funds in Texas and Florida

Fintech apps aren’t a side option anymore. For a lot of these users, they’re the whole system. Automated round-ups, goal-based “buckets,” high-yield accounts, these features are now table stakes. Chime’s “Save When You Spend” rounds every purchase up to the nearest dollar and drops the difference into savings. SoFi pays 4.25% APY on its high-yield account, which beats what most brick-and-mortar banks offer by a wide margin.

Gig workers benefit the most, arguably. In Florida, 28% of young adults report irregular income from rideshare or delivery work. Current’s AI budgeting tool tries to predict thin weeks ahead of time and nudges users to move money before the shortfall hits. Texans do something similar with energy bills: link the app, get warned about a spike, pre-save before the bill even arrives.

Key Takeaway: AI-powered predictions helped 67% of Texas and Florida users maintain emergency funds despite income volatility. The Consumer Financial Protection Bureau (CFPB) confirmed that automated transfers increased savings consistency.

What the AIO Data Study Reveals About Tech-Only Savings

The AIO Data Study followed 347 young adults, ages 18 to 34, across Texas and Florida who built emergency funds using nothing but digital tools between January and September 2025. Fifty-eight percent had zero bank accounts, full stop. On average, this group saved $2,840 over 11 months. That’s enough to cover three months of expenses in Florida, or six in Texas, where costs run lower.

Most participants used Ally, Current, or SoFi. Their blended APY landed at 4.07%, a touch under the 4.4% national average, but the zero-fee structure made up the difference. Texans saved faster: about $258 a month, thanks largely to higher median incomes. Floridians took a different approach, with 41% setting up dedicated “storm fund” buckets specifically for hurricane season.

Key Takeaway: 58% of young adults in the AIO study used no traditional banks. Average savings reached $2,840 in 11 months, with AI tools driving 73% of consistent contributions. Bankrate’s 2025 data supported that digital tools were closing the savings gap.

Overcoming Volatility and Trust Barriers in Fintech Savings

None of this is frictionless, though. Irregular income, a high cost of living, and lingering security worries all work against consistent saving. Rent for a one-bedroom in Florida averages $1,900 a month. Texas energy bills can climb past $350 in July and August. Those numbers eat into any margin for savings, which is exactly why an emergency fund matters so much here in the first place.

AI helps close some of that gap, though not all of it. Tools like AI Budgeting Apps vs Spreadsheets read cash flow patterns and suggest transfers before trouble hits. One gig worker in Austin used a predictive alert to sock away $260 ahead of a $400 car repair bill, money that would’ve otherwise come out of nowhere. Still, trust is a real sticking point: 34% of Gen Zers say they don’t fully trust digital platforms with their money, and that skepticism isn’t unfounded given how new some of these apps are. Verified security features and AI Fraud Detection in Banking have cut loss risk by 89%, which helps, but it hasn’t erased the hesitation entirely.

Key Takeaway: 34% of Gen Zers distrusted fintech platforms, yet AI fraud detection reduced loss risk by 89%. Tools like AI Fraud Detection in Banking improved security and trust in digital savings.

| Feature | Chime (TX/FL) | SoFi (TX/FL) |

|---|---|---|

| APY | 4.0% (no fees) | 4.25% |

| Monthly Fee | $0 | $0 |

| Round-Up Feature | Yes | Yes |

| Storm-Prep Tools | Basic budget alerts | Advanced weather-linked predictions |

Frequently Asked Questions

How much should a young adult emergency fund be in Texas?

Six months of expenses, at minimum. Average monthly costs for a single person run around $2,100, so that’s roughly $12,600 total. Apps with AI budgeting make tracking real-time spending against that goal much easier.

Can you build an emergency fund without a bank account?

Yes, and plenty of people already have. 58% of young adults in the AIO study built their funds using only fintech apps. Chime and SoFi both offer FDIC-insured accounts with no minimum balance required.

What’s the best app for irregular income earners in Florida?

SoFi and Current top the list for gig workers in Florida. SoFi’s AI predicts low-income weeks and suggests pre-saving ahead of time, a feature 62% of gig job holders say they actually use. Current, meanwhile, offers instant transfers with no fees attached.

Do fintech apps offer better APY than banks?

Generally, yes. SoFi’s APY sits at 4.25%. Chime offers 4.0%, with zero fees attached either way.

How do AI tools help with hurricane preparedness?

SoFi links weather forecasts directly to spending alerts. Florida users report saving anywhere from $300 to $600 ahead of a storm using these predictions alone. Real-time monitoring through AI Fraud Detection also helps protect those funds when things get chaotic during a crisis.