Our Take

For tech workers earning $300,000 to $600,000, traditional 401(k) contributions usually win in the years you’re actually earning that much. The deduction hits your top marginal bracket, often 32% to 37%. The case for Roth flips hard if you’re under 40, plan to retire early, or expect to relocate to a no-income-tax state. Once your FICA wages cross roughly $145,000, note that SECURE 2.0’s 2026 rule forces catch-up contributions into Roth regardless of preference.

Updated September 2025

The Roth versus traditional 401(k) question gets asked constantly by software engineers and product managers who just cleared six figures in base salary and are staring at an RSU vest that pushed them into a bracket they didn’t expect. It matters more in 2025 than it did five years ago. The 2025 employee deferral limit climbed to $23,500, per the IRS’s official 2025 contribution limits page. That’s real money to place in the wrong bucket for thirty years.

This piece is for high earners in tech, finance, or medicine making $300,000 or more who have both Roth and traditional options in their 401(k) plan. It’s for those who’ve hit the generic advice wall. The recommendation holds when your current marginal rate clearly exceeds your expected retirement rate. It breaks down for anyone planning an early exit from the workforce, or a move to a lower-tax state before drawing down the account.

Key Takeaways

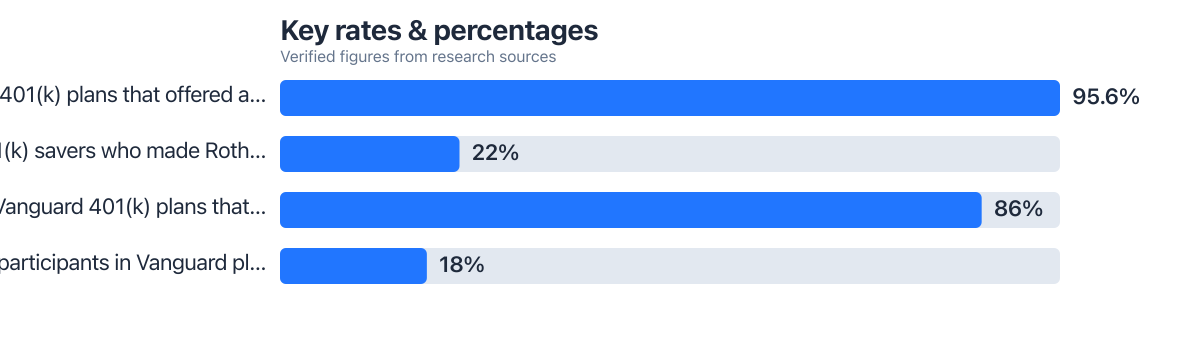

- Only 22% of 401(k) savers actually made Roth contributions in 2024, even though 95.6% of plans offered the option, according to the Plan Sponsor Council of America’s 2025 survey.

- The 2025 employee deferral limit is $23,500 for both Roth and traditional 401(k) contributions, per the IRS’s 2025 COLA table.

- In Vanguard-administered plans, 86% offered a Roth option by the end of 2024. Yet only 18% of eligible participants used it, based on Vanguard’s 2025 plan data.

- High earners who default to Roth “because it’s popular advice” without running their own bracket math leave real deduction value on the table in peak earning years.

- Starting in 2026, workers with prior-year FICA wages above roughly $145,000 must direct catch-up contributions to Roth, per IRS guidance on designated Roth accounts.

Why High-Income Tech Workers Face a Different Roth vs. Traditional Calculus

Standard retirement advice assumes a smooth income curve. Tech compensation doesn’t work that way. A senior engineer with a $220,000 base salary can see total income jump to $400,000 or more in a year when RSUs vest heavily. That jump often pushes marginal rates from 24% straight past 32% into 35%.

This income lumpiness breaks standard Roth vs. traditional 401(k) advice. The guidance built for a steady $90,000 salary doesn’t translate when your taxable income swings by six figures year to year. A traditional 401(k) contribution in a high-vesting year shelters income at the top marginal rate, 35%, not 22%. That’s a materially different trade.

What I see in practice: Clients who time traditional contributions to years with unusually large RSU vests capture a bigger deduction than those who split contributions evenly. The difference compounds when it’s a repeatable pattern across a four-year vesting cycle.

When the Rule of Thumb Fails

The old rule, contribute Roth when young, traditional when income peaks, still holds broadly. But it assumes retirement income will be lower. That’s not guaranteed for tech workers who retire early with large taxable brokerage accounts, rental income, or consulting work.

Dr. Jim Dahle, founder of White Coat Investor, puts a number on where the math shifts:

“If you have a very high income, which I usually define as $500,000–$2 million, you may prefer to make Roth contributions. It allows you to provide asset protection and tax-advantaged growth to more money on an after-tax basis, and if most of your income is going to be taxed at the highest tax rate in retirement, there is little advantage to withdrawing at your effective tax rate (since it is nearly the same as your marginal rate).”

That’s the exception to the general recommendation. It’s worth naming directly: above roughly $500,000 in stable, recurring income, the math for traditional weakens. There’s no lower bracket to fall into during retirement.

2025 Contribution Limits and the SECURE 2.0 Catch-Up Twist

The dollar limits are identical for both account types. This isn’t a capacity question. It’s a tax-timing one. In 2025, employees under 50 can defer up to $23,500 into either a Roth or traditional 401(k), or split between them, per the IRS’s official limits page. Workers 50 and older can add standard catch-up contributions.

Heads up for 2026 planning: Starting in 2026, SECURE 2.0 requires that catch-up contributions from anyone whose prior-year FICA wages exceeded roughly $145,000 go into a Roth account, not traditional. That means high earners at large tech employers should expect part of their next year’s catch-up bucket to lose its deduction value. 2025 is the year to plan around it.

This rule matters now. Plan administrators are already adjusting default elections ahead of the deadline. Workers who assumed they’d shelter catch-up dollars pre-tax indefinitely need to revisit that assumption. The IRS designated Roth account guidance covers the mechanics.

Where this gets tricky: Clients approaching 50 often assume the 2026 Roth catch-up mandate is years away and worth ignoring. But plan administrators are already resetting default elections in late 2025. Waiting until the rule takes effect to react means missing a full year of deliberate planning.

Running the Numbers: Tax Bracket Now vs. Retirement

Here’s the arithmetic that decides most cases. A worker earning $400,000 in taxable income sits in the 35% federal bracket in 2025. A $23,500 traditional contribution saves about $8,225 in taxes now, 35% of the contribution. A Roth contribution means paying $8,225 up front.

| Scenario | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| 2025 contribution | $23,500 pre-tax | $23,500 after-tax |

| Immediate tax cost at 35% bracket | $0 (deducted now) | ~$8,225 paid now |

| Value if retirement bracket stays 35% | Break-even | Break-even |

| Value if retirement bracket drops to 22% | Traditional wins | Roth loses value |

| Value if retirement bracket rises to 37%+ | Traditional loses value | Roth wins |

Break-even is simple: if your retirement tax rate equals your current marginal rate, the two accounts produce the same after-tax spending power. Traditional wins if retirement rates are lower. Roth wins if they’re the same or higher.

For most high earners, retirement income drops. Social Security and required minimum distributions rarely replace a $400,000 salary. But there’s a wrinkle. RMDs from a large traditional balance, combined with Social Security, can push retirees back into a higher bracket than expected. They can also trigger Medicare IRMAA surcharges, something Roth withdrawals never trigger, since they don’t count as taxable income.

What clients often miss: The IRMAA surcharge risk from a large traditional balance rarely shows up in a client’s mental model until we run a projected RMD schedule side by side with their Social Security estimate. Seeing the combined number in one table changes the contribution split more than any bracket argument does.

Roth 401(k) as the Only Tax-Free Path for High Earners

High earners get locked out of Roth IRA contributions once income crosses the phase-out range. That’s why the Roth 401(k) matters so much. Unlike a Roth IRA, the Roth 401(k) has no income limit. It’s the only direct route to tax-free retirement growth for someone earning $350,000 or more.

Mega backdoor Roth: Many large tech employer plans allow after-tax contributions beyond the $23,500 employee limit, up to the total plan cap, which can then be converted to Roth. This is one of the biggest gaps in generic advice: workers assume their Roth options stop at $23,500 when their plan may allow tens of thousands more in after-tax conversions.

Anyone weighing broader retirement strategy should also look at how a Roth IRA vs. traditional IRA comparison plays out alongside workplace accounts. The two often work best in combination, not isolation.

Where This Recommendation Falls Short

This isn’t a universal rule. Treating it as one is where people get burned. The traditional-first advice breaks down in three specific situations.

First: early retirement. Tech workers pursuing FIRE timelines often plan to stop working in their 40s or early 50s, well before age 59½. A large traditional balance becomes awkward to access early without triggering penalties. Roth contributions (though not earnings) can be withdrawn without penalty at any time. For this group, tilting toward Roth, even at a higher current marginal rate, buys flexibility the tax-rate comparison misses.

Second: state tax changes. A worker in California or New York paying combined state and federal rates near 45% to 50% gets a huge deduction from traditional contributions today. But if they retire in Texas, Florida, or Washington, withdrawals in retirement avoid state tax entirely. That strengthens the case for traditional, not weakens it. The risk? Assuming your current state tax rate will apply in retirement. Run the numbers with your planned retirement state, not your current one.

Third: large one-time expenses. If you expect a major expense soon, like a home purchase or business launch, reducing current taxable income via traditional contributions has direct cash-flow value Roth can’t match. Employer matches are always pre-tax, regardless of your election. That portion behaves like a traditional account no matter what.

And not for everyone: if your plan doesn’t offer a Roth option (still roughly 4.4% of plans as of late 2024, per the PSCA’s 2025 data), this whole framework is moot until you change jobs or your employer adds the feature.

How to Decide in 2025

Run three checks before you set your contribution election. Let the answers, not a default habit, decide the split.

First: what’s your marginal rate this year? Factor in RSU vesting and bonus timing, not just your base salary.

Second: do you have a real, planned path to a lower-tax state or reduced income before touching this money?

Third: are you within ten years of retirement age, or targeting an early exit that makes penalty-free access more valuable than the deduction?

Dr. Dahle’s rule of thumb captures the mainstream case well:

“I only have one rule of thumb, and it’s that residents (and military docs) should make Roth contributions and attendings should generally make traditional, tax-advantaged contributions. But there are plenty of exceptions to that rule.”

Translate that to tech: junior engineers early in their careers, likely in the 22% to 24% bracket, should lean Roth. Senior engineers, staff engineers, and directors earning $350,000-plus in a peak vesting year should lean traditional, unless they’re planning early retirement or a move to a lower-tax state. In which case, Roth deserves a larger share, even at the higher current rate.

Workers managing both RSU income and 401(k) elections often benefit from the kind of systematic tracking discussed in how to start investing for retirement when you’re in your 40s. The contribution-timing decision doesn’t happen in isolation.

Quick gut check: If your combined federal and state marginal rate today is above 35% and you expect to retire in a lower-tax state with a smaller income, traditional wins. If you’re under 40, expect an early exit, or your rate today is at or below 24%, Roth wins.

Case Study: A Staff Engineer’s Mid-Vesting Split

A staff engineer at a mid-sized cloud software company came to us earning a $240,000 base salary. An RSU vest pushed total taxable income to roughly $410,000 in 2024. He’d been splitting 401(k) contributions 50/50 for three years, following advice that “diversification” of tax treatment was safe.

Running his actual marginal rate for the vest year showed he was solidly in the 35% federal bracket. No planned relocation. No early retirement target before 55. We shifted his election to fully traditional for 2025. The full deduction landed at his top bracket. He kept his existing Roth balance untouched. Preserved tax diversification from prior years. Directed new dollars where the current-year math favored it.

The change was projected to increase his effective annual tax savings by roughly $2,900 compared to continuing the 50/50 split. Based on his 2025 marginal rate and contribution amount.

Setting Your 2025 Election

- Pull your actual projected taxable income for 2025, include expected RSU vesting and bonus timing, not just base salary.

- Identify your marginal federal and state bracket for that income. Compare it honestly to your expected retirement-year bracket.

- Check whether you’re within ten years of retirement, planning an early exit, or expecting a move to a lower-tax state. Any of these shift the recommendation toward Roth.

- If your plan offers a mega backdoor Roth, confirm the after-tax contribution and in-plan conversion mechanics with your plan administrator before year-end.

- If you’re 50 or older, review how the 2026 Roth catch-up mandate will affect your contribution structure next year. Adjust your 2025 traditional vs. Roth balance accordingly.

- Revisit your election at least once mid-year if your compensation includes variable RSU vesting. A single annual decision often misses a mid-year income jump.

How We Sourced This

This article draws from the IRS’s official 2025 contribution limit tables and designated Roth account guidance, the Plan Sponsor Council of America’s 2025 survey on Roth plan adoption, Vanguard’s 2025 participant behavior data as reported by Carry, and direct commentary from Dr. Jim Dahle of White Coat Investor. Data covers plan years through the end of 2024 and IRS limits published for 2025, with no figures dated after September 2025. Statistics were selected for direct relevance to high-income contribution decisions and cross-checked against the original publishing organization’s page. Sources were last verified in September 2025.

Common Questions

Should high-income earners choose Roth or traditional 401(k) in 2025?

Most high earners above $350,000 in stable annual income benefit more from traditional contributions in 2025. The deduction lands at their top marginal rate. The exception is anyone planning early retirement, a move to a no-income-tax state, or already earning above $500,000, where Roth’s tax-free growth outweighs the upfront deduction.

What is the 401(k) contribution limit for 2025?

The employee deferral limit is $23,500 for 2025, applying equally to Roth and traditional contributions, according to the IRS’s contribution limit table. Catch-up contributions for those 50 and older add to that base figure.

Do high earners have to make Roth catch-up contributions starting in 2026?

Yes. Workers whose prior-year FICA wages exceeded roughly $145,000 must direct catch-up contributions to a Roth account starting in 2026 under SECURE 2.0. This removes the pre-tax deduction on that portion of contributions for affected high earners going forward.

Can high earners contribute directly to a Roth IRA instead of a Roth 401(k)?

No. Direct Roth IRA contributions phase out at income levels well below what most senior tech workers earn. The Roth 401(k) has no income limit. It’s the practical route to tax-free growth for anyone locked out of a Roth IRA.

What is a mega backdoor Roth and who can use it?

A mega backdoor Roth lets employees contribute after-tax dollars beyond the standard $23,500 limit, up to the total plan cap, then convert those dollars to Roth. It’s only available if your specific employer plan permits after-tax contributions and in-plan conversions, common at large tech companies, but far from universal.

Does an employer 401(k) match count as Roth or traditional?

Employer matching contributions are always treated as pre-tax, traditional dollars, regardless of which account type the employee chooses. That match grows tax-deferred and gets taxed on withdrawal, just like a traditional employee contribution.

Is it worth splitting contributions between Roth and traditional 401(k)?

Splitting makes sense for workers with volatile income who want tax diversification without betting entirely on one future tax rate. A common approach is directing contributions traditionally during high-vesting years and shifting toward Roth in lighter-income years. This smooths the tax-timing bet across a career instead of locking into one account type permanently.

Sources

- Internal Revenue Service: 2025 Contribution Limits

- Internal Revenue Service: Designated Roth Accounts in 401(k) or 403(b) Plans

- Internal Revenue Service: Publication 4530 – Designated Roth Accounts

- Dr. Jim Dahle, MD, White Coat Investor: Roth vs. Traditional 401(k) Contributions

- Plan Sponsor Council of America: 2025 Roth Option Offerings Survey

- Carry: 2025 401(k) Participant Behavior Data (Vanguard)

- Internal Revenue Service: Roth Comparison Chart

- Internal Revenue Service: FAQs on Designated Roth Accounts

- Internal Revenue Service: Rollovers and Tax Treatment of Retirement Plans

- Internal Revenue Service: Qualified Retirement Plans Overview

- Internal Revenue Service: 401(k) Account Rules and Limitations

- Internal Revenue Service: Medicare IRMAA and Taxable Income

- Internal Revenue Service: Required Minimum Distributions (RMDs)

- Internal Revenue Service: SECURE 2.0 Act Summary

- Internal Revenue Service: 401(k) Rollovers and Distributions