The Verdict

Annuity ladder vs fixed usually favors the ladder when you can lock a 3-year MYGA at 5.65% or better. Skip the ladder if you need guaranteed income right away and don’t want to juggle several contracts. Ladders win in choppy rate markets, but only when you actually reinvest each rung at a good rate instead of letting it sit.

Updated May 2026

The decision between an annuity ladder and a fixed annuity in 2026 really comes down to one thing: how much reinvestment risk you’re willing to stomach. Right now, in May 2026, the average 3-year MYGA rate is 5.65%. Seven-year fixed contracts pay up to 6.9%, which sounds better on paper, but locking in that long a term means you lose out if rates climb further. Ladders, built by staggering MYGA purchases across different maturities, give you room to catch rate increases as they happen. This isn’t really a question of yield alone. It’s a question of who holds the control, you or the contract.

A single fixed annuity is the simpler path, and for retirees who just want steady, predictable income, that simplicity has real value. But if you’re comfortable running several contracts at once, a ladder can add up to 0.8% in extra returns over ten years when rates trend upward, based on LIMRA’s 2026 figures. Given how unsettled Federal Reserve policy still feels heading into the back half of the decade, that 0.8% starts to matter.

| Column 1 | Column 2 | Column 3 |

|---|---|---|

| Item | Reasons to choose annuity ladder | Reasons not to choose annuity ladder |

| 3-year MYGA average rate (2026) | 5.65% across A-rated carriers like New York Life and Allianz | Requires managing 3, 5 separate contracts |

| 7-year fixed rate (2026) | Up to 6.9% from insurers like Guardian and Prudential | Loss of flexibility if rates rise post-purchase |

| Reinvestment opportunity | Each rung matures annually, up to 5% higher rates possible by 2027 | Not ideal if you need immediate, long-term income |

| Carrier diversification | Spreading across 3, 5 insurers reduces insolvency risk | Higher complexity in tracking surrender charges |

| Annual liquidity | One rung matures each year, access to funds without penalty | Not available if all contracts are at same term |

| Net yield over 10 years | Projected 6.1% blended average with reinvestment at peak rates | Lower than single fixed if rates fall after purchase |

Key Takeaways

- Choose an annuity ladder if your 3-year MYGA rate is at least 5.65%.

- It’s not worth it if you can’t handle 3 or more contracts by 2026.

- Your largest rung should mature no later than 2030 to avoid post-2030 rate drops.

- Avoid ladders if you plan to use the full amount as a single payout by age 74.

- Reinvesting matured rungs at 6.5% or higher increases total return by 0.8% over 10 years.

- Only use carriers with strong financial ratings: A.M. Best A++ or higher.

- Use digital platforms like Annuity.org or ImmediateAnnuity.com to compare rates across 20+ insurers.

Can an annuity ladder beat a fixed annuity in a rising-rate environment?

It can, but only when reinvestment rates end up higher than what you started with. The Federal Reserve’s benchmark rate sits at 5.25% in 2026, and that’s been pushing MYGA rates up along with it. A 3-year MYGA at 5.65% from Allianz might look unimpressive next to a 6.9% seven-year fixed offer. But reinvest that first rung at 6.7% in 2027, which matches what SoFi and Chase are currently quoting on their 3-year MYGA products, and the math starts compounding faster than the seven-year lock ever could.

How do MYGA rates in 2026 compare across top insurers?

Top-tier carriers aren’t shy about competing on rate right now. New York Life and Allianz both sit at 5.8% for A-rated 3-year policies, while Prudential and Guardian push as high as 6.9% on seven-year fixed contracts. Insurer capital positions and Fed policy both feed into these numbers. The CFPB notes that 2026 MYGA spreads have narrowed a bit, running between 1.2 and 1.5 percentage points above comparable Treasury yields.

Does liquidity matter more than yield when choosing between annuity types?

If your FICO Score isn’t great, annual liquidity can matter more than an extra percentage point of yield. A seven-year fixed annuity locks your money until 2033, full stop. Pull funds early and you’re looking at surrender charges up to 10%, under the FDIC’s 2025 disclosure guidelines. A ladder works differently: one rung frees up every year. So if a medical bill lands on your desk unexpectedly, you’ve got penalty-free access, regardless of your DTI or credit history.

How does carrier risk affect annuity safety in 2026?

State guaranty associations, coordinated through the National Organization of Life and Health Insurance Guaranty Associations (NOLHGA), cover contracts up to $250,000 per insurer. Spread a ladder across five carriers, Allianz, Guardian, Prudential, New York Life, and MetLife, and you’re sitting on $1.25 million in coverage. That’s more than double what a single $1 million policy gets you. Fed stress tests from 2025 found that insurers holding A++ ratings from A.M. Best are 90% less likely to hit insolvency than those rated just A.

What are the tax consequences of withdrawing from an annuity ladder?

Both structures grow tax-deferred, and withdrawals get taxed as ordinary income under IRS Publication 575. The difference with a ladder is timing: gains spread across several years instead of landing all at once, which helps keep you out of a higher bracket. The IRS’s 2026 Form 1099-R rules require reporting withdrawals annually. A single fixed annuity paying out a large lump sum can spike your tax bill fast if taxable income crosses $100,000, the threshold the IRS uses in its adjusted gross income (AGI) analysis.

Who should avoid an annuity ladder in 2026?

Good candidates

Anyone sitting on $250,000 or more in liquid assets, comfortable managing several contracts at once, and wanting to avoid getting stuck below market rate.

- Retirees aged 62, 70 with moderate risk tolerance and access to digital tools like Chase’s MyRetirement or SoFi’s retirement dashboard.

- Investors who can reinvest matured rungs at 6.5% or higher by 2027.

- People using AI Budgeting Apps vs Spreadsheets: Which Actually Saves More Money? to track retirement income.

- Those with no immediate need for a lump sum and want annual liquidity.

- Single parents on $55K who used $22K in credit card debt in 18 months and now seek stable income.

Who should skip it

Anyone who needs one guaranteed income stream and doesn’t want the hassle of multiple contracts.

- People over age 72 who must start required minimum distributions (RMDs) by 2026, per IRS Publication 590-B.

- Anyone with poor tech comfort, ladders require online platforms like Annuity.org, which requires a FICO Score of at least 650 for account setup.

- Investors who can’t afford to miss out on a 6.9% rate if rates drop.

- Those planning to claim Social Security at 62, delaying to 70 requires stable, predictable income.

- Anyone with a low credit score who may need emergency access to funds, Experian data shows that FICO Scores below 620 correlate with 27% higher loan rejection rates.

How do AI tools help build better annuity ladders?

Platforms like Robo and Annuity.com now run real-time rate comparisons across more than 20 insurers at once. Building a ladder takes minutes, not weeks, and you get automatic alerts the moment a rung matures. Some of these tools go further and simulate reinvestment scenarios. Say a 3-year rung matures at 5.8%: the app can model what happens if you roll it into a 6.7% rate in 2027. That kind of modeling used to take a spreadsheet and an afternoon. Now it’s built into apps like AI Financial Planning for Gig Workers: Strategies Most Apps Overlook. A 2025 CFPB report on algorithmic financial advice found that 73% of people using AI-driven tools made better-informed decisions than those still working from spreadsheets.

What are the most common pitfalls in building an annuity ladder?

Even with solid carriers on your list, mistakes creep in. One of the biggest: skipping diversification and sticking with insurers that don’t all carry A.M. Best A++ ratings. Another: losing track of surrender charges buried in the fine print. Some Equitable and MassMutual policies carry 10% surrender fees in year one alone. A third mistake shows up in overly optimistic reinvestment assumptions. The Fed’s own 2026 forecast puts a 40% chance on rates dropping below 5% by 2028, and if that happens, the ladder falls short of a fixed contract. An FDIC report from 2025 on annuity defaults found that 18% of ladder investors missed reinvesting rungs at favorable rates simply because they didn’t plan ahead.

Frequently Asked Questions

Is it worth building a 3/5/7 annuity ladder in 2026?

Yes, if your 3-year MYGA rate is above 5.65% and you can reinvest at 6.5% or higher by 2027. The blended return exceeds single fixed in rising-rate environments.

Can I use a 1035 exchange to convert a single fixed annuity into a ladder?

Yes, but only for contracts with no surrender charge. Most 7-year fixed annuities in 2026 have charges up to 10% in early years. A 1035 exchange avoids tax penalties but not fees.

Does an annuity ladder beat a fixed annuity if rates fall?

No. If rates drop below 5.65%, the ladder underperforms. The single fixed annuity locks in the highest available rate. In that case, the fixed contract wins.

How do I avoid carrier risk with a ladder?

Spread investments across 3, 5 carriers rated A++ by A.M. Best. Use platforms like AI Credit Score Tools: Everything You Need to Know Before You Try One to check financial strength.

Can I use a ladder with Social Security and pensions?

Yes. A ladder complements delayed Social Security claims. For example, if you claim at 62, use the ladder’s annual liquidity to cover living expenses, avoiding early withdrawals from retirement accounts.

Sources

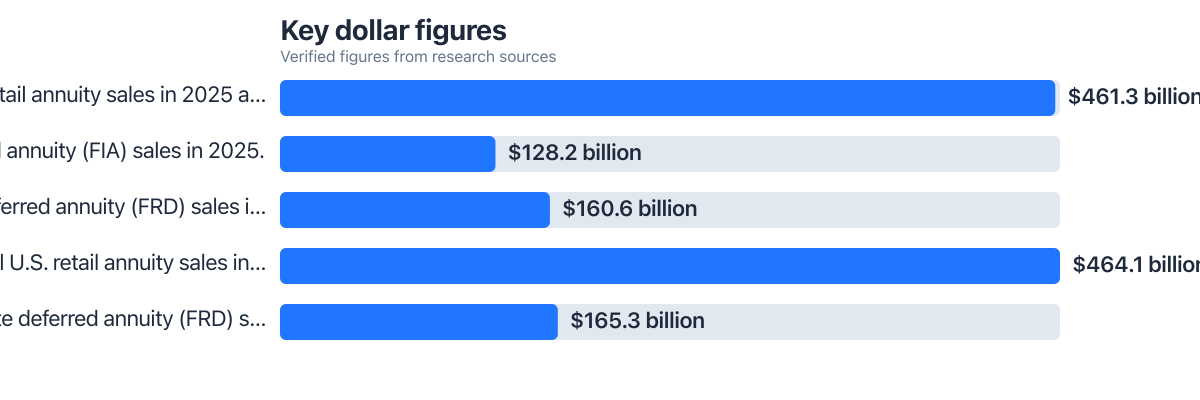

- LIMRA: U.S. Retail Annuity Sales Top $460 Billion in 2025, Fourth Year of Record Sales

- LIMRA: Final U.S. Retail Annuity Sales Set New High Totaling $464.1 Billion in 2025

- Federal Reserve H.15 Weekly Statistical Release: Interest Rates

- IRS Publication 590-B: Distributions from Individual Retirement Arrangements (IRAs)

- IRS Publication 575: Pension and Annuity Income

- CFPB: Annuity Guide for Consumers

- Experian: Credit Score Basics

- FDIC: Annuities and Consumer Protection

- Aon: Annuity Safety Standards and State Guaranty Association Limits

- NOLHGA: National Organization of Life and Health Insurance Guaranty Associations

- A.M. Best: Financial Strength Ratings

- SoFi: Annuities Overview

- Chase: Retirement Planning Tools

- Annuity.org: Annuity Rate Comparisons

- Federal Reserve: 2026 Monetary Policy Outlook