Quick Answer

To pay rent in New York City without a bank account, use cash-friendly platforms like RentRedi for retail deposits, card-splitting apps like Kasheesh or Flex for flexible timing, and prepaid debit cards to receive gig income. Roughly 7.6 percent of New Yorkers are unbanked, and most tools take 10 to 20 minutes to set up once you have a government ID and a phone number.

Updated July 2026

Here’s what the data shows: paying rent without a checking account in New York City is harder than it should be, but it is no longer impossible. Renter fintech tools built around cash deposits, prepaid cards, and split-payment apps now let unbanked tenants pay landlords who still expect ACH transfers or paper checks. The city’s own comptroller found that 7.6 percent of New Yorkers reported being unbanked in 2023, well above the national rate, according to a 2025 New York City Comptroller report.

Rent in most boroughs keeps climbing this year, while landlord payment systems haven’t caught up to how unbanked renters actually manage money. Roughly 67.3 percent of New York City households are renters, per the NYU Furman Center’s 2026 State of the City report, and a meaningful slice of that population works gig jobs, gets paid in cash, or simply distrusts traditional banks after past overdraft fees. Some of that distrust traces back to the same fee and disclosure issues the Consumer Financial Protection Bureau has flagged for years at large retail banks like Chase and Bank of America. Nonbank payment apps have already gone mainstream; nearly half of U.S. households, 49.7 percent, used services like PayPal, Venmo, or Cash App in 2023, according to the FDIC’s 2023 household survey.

This guide is for renters in the five boroughs who lack a checking account, whether by choice, immigration status, credit history, or bank access barriers, and who need a working method to pay a landlord on time every month. By the end, you’ll know which apps accept cash, which ones split payments across prepaid cards, and which credit-building tools are actually usable without a traditional bank behind them.

Key Takeaways

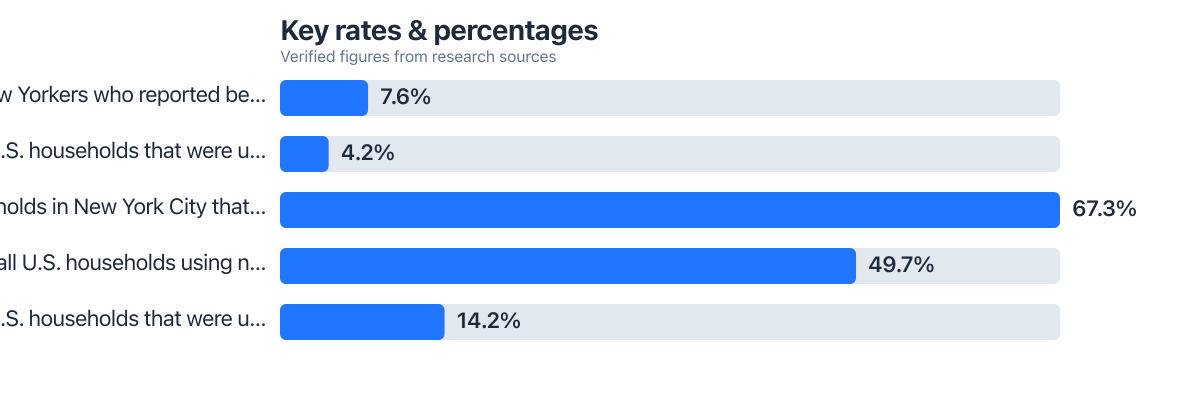

- 7.6 percent of New Yorkers reported being unbanked in 2023, a rate higher than the national average, according to the New York City Comptroller.

- Nationally, 4.2 percent of U.S. households, or 5.6 million households, were unbanked in 2023, per the FDIC.

- 67.3 percent of New York City households rent rather than own, per the NYU Furman Center, meaning a huge share of the city depends on some form of rent-payment workaround.

- 49.7 percent of U.S. households already use nonbank payment apps like Venmo or Cash App, per the FDIC, showing these tools are mainstream, not fringe.

- 14.2 percent of U.S. households, 19.0 million total, are underbanked, meaning they have an account but still rely on alternative financial products, per the FDIC.

- RentRedi advertises cash payments accepted at retail locations specifically for tenants without a bank account, a feature most competing rent apps bury as an afterthought.

In This Guide

- Step 1: Why Rent Is Hard to Pay Without a Bank Account in NYC

- Step 2: What Makes a Fintech Tool Actually Bank-Free?

- Step 3: How Flex and Kasheesh Handle Rent

- Step 4: Paying Rent With Cash Through RentRedi

- Step 5: Can Rent Payments Build Credit Without a Bank?

- Step 6: Do NYC Landlords Have to Accept These Tools?

- Step 7: How to Start Safely and Avoid Scams

Step 1: Why Rent Is Hard to Pay Without a Bank Account in NYC

Most New York City landlords still expect rent through a bank transfer, a personal check, or a certified check drawn on a checking account. That locks out anyone without one. The gap is bigger here than in most of the country: 7.6 percent of New Yorkers reported being unbanked in 2023, compared with a national unbanked rate of 4.2 percent, or 5.6 million households, according to the FDIC’s 2023 survey and the city Comptroller’s 2025 analysis.

The renters hit hardest tend to be recent immigrants without a Social Security number or ITIN, tenants who’ve had a past eviction or bank account closure, and gig workers whose income doesn’t fit neatly into a pay-stub verification form. Property managers in Manhattan and Brooklyn frequently require proof of a checking account just to apply for an apartment, which pushes unbanked renters toward money orders or landlords willing to take cash directly, an option shrinking as more buildings switch to digital-only portals. Even renters with decent income and a strong FICO Score can hit this wall if they simply don’t hold a traditional account at a bank like Chase, Citibank, or a credit union.

Step 2: What Makes a Fintech Tool Actually Bank-Free?

A renter fintech tool works without a bank account when it lets you fund payments with cash, a prepaid debit card, or a payroll card, and when it doesn’t require a checking account just to create a profile. Look for three things before signing up: a cash deposit network, a prepaid card option, and no hard requirement for a linked ACH account.

Fee structure matters just as much as access. A tool that accepts cash but charges 3 percent per transaction can quietly cost more over a year than a subscription-based splitter with a flat monthly fee. The math only works in your favor if you actually use the credit-building or scheduling features enough to offset the cost, similar to how a rewards credit card only pays off if you clear the balance and avoid the card’s APR.

How to Do This

Start by checking whether the app lists a cash deposit partner network, such as retail locations for adding funds, rather than only using “cash” as marketing language while requiring a bank link on the back end. Confirm the app supports prepaid Visa or Mastercard debit cards, since many gig platforms and government benefit programs issue funds this way. If you’re building a broader financial picture beyond rent, tools covered in this guide on how freelancers can use fintech apps to replace a business bank account apply the same logic to income management, and some of those platforms, like SoFi, market themselves as an alternative to a traditional checking account entirely.

What to Watch Out For

Some apps advertise themselves as bank-free but still require you to link a debit card tied to an existing checking account during onboarding. Read the fine print on “supported funding methods” before assuming cash or prepaid cards will actually work for your specific landlord’s payout preference. And if your credit file is thin or nonexistent, a few of these tools pull a soft check through Experian or TransUnion during signup, which can add friction even when no bank account is required.

Nearly half of all U.S. households, 49.7 percent, already used nonbank payment services like PayPal, Venmo, or Cash App in 2023, according to the FDIC. Renter-focused apps are simply extending that same behavior to a monthly rent bill instead of splitting a dinner check.

Step 3: How Flex and Kasheesh Handle Rent

Flex and Kasheesh both let you split one rent bill across multiple payment dates or multiple cards. That helps renters without steady bank deposits smooth out cash flow, but neither is a true no-bank-account solution on its own. Flex charges a recurring membership fee of up to $14.99 per month plus a 1 percent bill payment fee, and it runs a credit assessment, similar to how a lender checks your DTI ratio before approving a loan, which limits access for renters without an established credit file. Kasheesh allows splitting a rent payment across multiple cards, including some prepaid cards, but the landlord still has to accept card payments in the first place, which many NYC buildings don’t.

Step 4: Paying Rent With Cash Through RentRedi

RentRedi stands out among rent-payment apps because it explicitly advertises cash payments accepted at retail locations for tenants who don’t have a bank account. You add funds at a participating retail partner, and the app routes the payment to your landlord electronically. No checking account, no linked debit card, needed.

Most competing platforms, including popular property management tools like Buildium and Avail, default to ACH bank transfers and treat cash as a minor add-on feature rather than a core option. RentRedi also supports prepaid debit cards for renters who receive gig income or public benefits on a reloadable card, making it one of the few tools built around the actual habits of unbanked New Yorkers rather than assuming everyone banks with an institution like Wells Fargo or Chase.

How to Do This

Create a tenant profile with your government ID and phone number, then locate a nearby cash deposit partner through the app’s retail network before your rent due date. Confirm with your landlord ahead of time that they’re set up to receive RentRedi payments, since the landlord side of the platform requires its own enrollment.

What to Watch Out For

Cash deposit networks charge a small fee per transaction at the retail counter, separate from any RentRedi platform fee, so factor both into your monthly rent cost. Processing can also take one to two business days longer than a same-day bank transfer, which matters if you’re paying close to a grace period deadline. If your landlord needs same-day confirmation or refuses to enroll in the platform at all, RentRedi simply won’t work for your situation, no matter how well it fits everything else.

Landlord acceptance is not guaranteed just because a fintech app supports cash or card payments. Confirm with your property manager, in writing, that they’ll accept the payment method before you rely on it for a rent due date with a late fee attached.

Step 5: Can Rent Payments Build Credit Without a Bank?

Yes. Several rent-reporting tools will report your on-time payments to credit bureaus, including Experian and TransUnion, even if you fund those payments through cash or a prepaid card rather than a checking account. Bilt Rewards is the best-known example, letting renters earn points and build payment history without requiring a specific bank relationship, though you still need some funding method the platform accepts.

The appeal of rent reporting is real, but it’s also the most crowded part of this market. The differentiator for unbanked renters isn’t whether a tool reports to bureaus. It’s whether that tool actually lets you fund the payment without a checking account in the first place. A lot of coverage treats rent-reporting and bank-free access as the same conversation; they aren’t. You can have a rent-reporting app that still requires ACH, which does nothing for someone without a bank.

Run the actual numbers before committing to a paid credit-building plan. Say you’re comparing a $12-per-month rent reporting subscription against a free app that reports without a monthly fee: over 18 months, the paid option costs $216 out of pocket, and that only makes sense if the FICO Score lift translates into a lower interest rate on something like a car loan or a credit card with a better APR down the line. If your near-term goal is just paying rent reliably, prioritize access over rewards points.

For a broader view of how automated credit tools evaluate renters and gig workers with thin credit files, see this guide on AI credit score tools, which explains what these systems weigh beyond a traditional bank account.

Before paying for any rent-reporting subscription, check whether your building’s property manager already reports payments through a service like Esusu or Rhino at no cost to tenants. Many NYC landlords added this after 2023 to reduce turnover, which means you might get the credit benefit without paying a third-party app at all.

| Tool | Cash or Prepaid Support | Monthly Cost | Credit Reporting |

|---|---|---|---|

| RentRedi | Yes, cash at 90,000+ retail locations | Landlord-paid; tenant fee varies by retail partner | Optional add-on |

| Flex | Limited; requires linked card | Up to $14.99 plus 1% bill fee | No |

| Kasheesh | Yes, splits across prepaid cards | Varies by card issuer, no flat fee | No |

| Bilt Rewards | Requires funding source, often a card | Free membership | Yes |

Step 6: Do NYC Landlords Have to Accept These Tools?

No. New York City doesn’t mandate that landlords accept cash, card, or app-based rent payments; acceptable payment methods are set in the lease itself, so confirm your specific method in writing before relying on it. Rent-stabilized units and buildings enrolled in HPD programs sometimes have additional payment documentation requirements tied to city recordkeeping, which can slow down onboarding for a new fintech tool compared with a market-rate apartment.

Renters using housing vouchers, including Section 8, should check with their caseworker before switching payment platforms, since voucher administrators typically require the subsidized portion of rent to move through a specific, pre-approved channel rather than a third-party app. This is one group that should be cautious here: switching a subsidized payment channel without prior approval can create a documentation headache with HPD or a local housing authority, even if the fintech tool itself works fine. If you’re also managing household budgeting decisions alongside a rent-payment switch, this comparison of AI budgeting apps versus spreadsheets covers how to track irregular cash-based income against a fixed rent obligation.

14.2 percent of U.S. households, 19.0 million total, were underbanked in 2023, meaning they had an account but still relied on alternative products like money orders or prepaid cards, according to the FDIC. That’s a much larger group than the fully unbanked population, and many renter fintech tools serve both groups at once.

Step 7: How to Start Safely and Avoid Scams

Set up your account directly through the official app store listing or the platform’s verified website, never through a link sent by a landlord or a third party claiming to process rent on their behalf. Legitimate renter fintech tools never ask for your full Social Security number to simply add cash funds. If a platform requests that level of detail before you’ve even confirmed a landlord partnership, treat it as a red flag. The Federal Reserve and the CFPB both publish consumer alerts on rent-payment scams targeting exactly this kind of onboarding step.

Keep a digital receipt or confirmation number from every cash deposit, since disputes over “my landlord never received the payment” are the most common complaint among unbanked renters using these tools. For newcomers building a broader financial foundation without prior U.S. credit history, pairing a rent-payment tool with insights from this guide on financial planning strategies most apps overlook for gig workers can help you sequence which accounts and tools to open first.

Related reading: AIO Decision: Should You Use a Fintech App for Emergency Fund Management in ?.

Frequently Asked Questions

Can I pay rent in NYC with only cash and no bank account?

Yes, through a platform like RentRedi, which routes cash deposited at partner retail locations to your landlord electronically. You’ll need your landlord to be enrolled in the same platform, so confirm compatibility before your first rent due date.

Do I need a Social Security number to use a rent-payment app in New York City?

Most rent apps require some form of government-issued ID, but requirements vary by platform, and some accept an ITIN instead of a Social Security number. Contact the specific app’s support team directly, since policies here change more often than the marketing pages reflect.

Which renter fintech tools actually work without a checking account?

RentRedi and Kasheesh come closest, since both support cash or prepaid card funding rather than requiring a linked bank account. Flex, by contrast, runs a credit check and functions more like a bill-splitting service than a true bank-free solution.

Will using a rent-splitting app hurt my chances of renting an apartment in NYC?

No, using a rent-splitting app to fund payments generally doesn’t appear on your rental application unless the app itself reports account activity to a screening service. Landlords typically only see whether rent arrives on time, not which tool you used to send it.

How much does it cost to pay rent with cash through RentRedi?

Costs vary by retail partner and typically include a small per-transaction fee separate from any platform charge, so check the fee display at the retail counter before completing the deposit. Compare that fee against a money order’s typical cost at a local check-cashing store to see which is actually cheaper for your situation.

Should I use Bilt Rewards if I don’t have a bank account?

Bilt Rewards can work, but you’ll still need a funding method the platform accepts, so it solves credit-building rather than the bank-account gap on its own. Pair it with a prepaid card or a cash-friendly funding option if you don’t have a checking account.

What happens if my landlord doesn’t accept fintech rent payments?

You’ll need to ask directly whether they’re willing to enroll in the specific platform you’re using, since acceptance is voluntary and varies building by building. Some tenants resolve this by requesting the landlord accept a money order instead while the fintech option gets set up.

Are prepaid debit cards a good way to pay rent if I’m a gig worker without a bank account?

Prepaid cards work well for gig workers because platforms like DoorDash, Uber, and Instacart often pay out to reloadable cards directly. Just confirm the card issuer allows recurring bill payments and check for reload fees, which can add up if you’re depositing cash to the card frequently.

Can immigrants without a Social Security number build credit through rent payments in NYC?

Some rent-reporting services accept an ITIN in place of a Social Security number, though not all bureaus, including Experian and TransUnion, process ITIN-based files the same way a standard credit file works. Check directly with the specific rent-reporting service and consider asking a housing counselor familiar with immigrant tenant issues in your borough.

Sources

- New York City Comptroller, Access to Banking and Credit in New York City (2025)

- Federal Deposit Insurance Corporation, 2023 FDIC National Survey of Unbanked and Underbanked Households

- NYU Furman Center, State of Renters and Their Homes 2025

- U.S. Department of Housing and Urban Development, Housing Choice Voucher Program

- NYC Department of Housing Preservation and Development, Official Site

- NYC Rent Guidelines Board, Official Site

- Wikipedia, Unbanked (Overview and Definitions)

- Consumer Financial Protection Bureau, Newsroom and Consumer Alerts

- Federal Deposit Insurance Corporation, Consumer Resource Center