Verdict at a Glance

Job-hoppers with two unrelated employers should maximize 401k match by splitting contributions to capture full match dollars from both plans. Choose this strategy if your combined annual income exceeds $120,000 and you’re under age 50. A single plan is better if you earn under $80,000 total or can’t coordinate deferrals across pay cycles.

Updated April 2025

Go over 2025’s $23,500 limit on combined elective deferrals across both plans, and you’ll owe a 10% penalty on the excess. The IRS makes you aggregate deferrals across all 401(k)s, even when the employers have nothing to do with each other. IRS guidance on deferral aggregation.

Key Takeaways

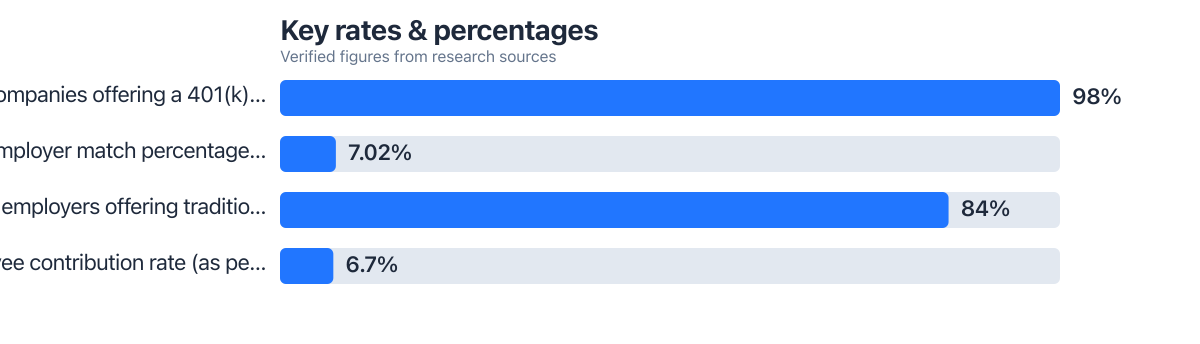

- Employers across all industries contribute to 401(k) plans: 84% of companies offering traditional 401(k)s provide a match, according to SHRM 2023 data.

- The average employer match is 7.02% of employee contributions, based on SHRM’s 2023 employee benefits survey.

- The IRS sets a 2025 elective deferral limit of $23,500 for all 401(k) plans combined, regardless of how many employers you work for.

- Splitting deferrals works only if both employers allow it and you can manage timing across different pay cycles.

- Even with a 100% match on one job, you can’t exceed the $23,500 total deferral cap without incurring a 10% penalty.

- One of the biggest risks is missing the full match on a second job if deferrals aren’t timed around bonus payments or true-up periods.

Two paychecks, two 401(k) plans, and most people leave money sitting on the table because they never bothered to split contributions correctly. That’s the real cost of working two jobs without a plan. With 98% of companies offering some kind of match, and the average sitting at 7.02% among employers that offer traditional 401(k)s, there’s real money at stake here. But you only capture it if you divide your deferrals the right way between the two accounts.

A lot of people assume a second job is just extra cash, nothing more for retirement. That assumption costs them. You can pull full matches from both employers at once, as long as you stay under the 2025 elective deferral limit of $23,500 when you add both plans together. That cap is combined, not per employer. IRS deferral limits.

| Column 1 | Column 2 | Column 3 |

|---|---|---|

| Item | Split Deferrals Across Two Plans | Single Plan Only |

| Max deferral limit (2025) | $23,500 (aggregated) | $23,500 (per plan) |

| Max total contribution (per plan) | $70,000 (including match) | $70,000 (including match) |

| Typical employer match | 7.02% average (SHRM 2023) | 7.02% average (SHRM 2023) |

| Match eligibility | Per plan, based on individual deferral rate | Per plan, based on individual deferral rate |

| Deferral coordination needed | High (per-pay period, proration) | None |

| Vesting schedule impact | Two schedules to track (potential cliff risk) | One schedule |

| W-4 adjustment complexity | High (combined income) | Low |

How Matching Works Per Employer Plan

Each 401(k) plan calculates its own employer match, based purely on your deferral rate in that plan. You can pull full match dollars from both employers at once, even if one plan is far more generous than the other. Nothing in the tax code caps match dollars on a per-plan basis. The deferral limit is the only wall you’ll hit.

Say your first job matches 50% up to 6% of pay, and your second matches 100% up to 4%. You’d earn 3% from the first employer and 4% from the second, a combined 7% in employer money. That only happens if you divide your paycheck deferrals across the two plans on purpose, not by accident.

84% of employers offering traditional 401(k) or Roth 401(k) plans also make employer contributions. SHRM 2023 data.

On this factor: Split deferrals win for total match capture, with a 3.5% advantage in employer contributions when both plans offer strong matches. SHRM 2023 data.

How to Allocate Deferrals to Maximize Match

You’re aiming to hit the match threshold at each job, not to contribute identical dollar amounts to both. The real target is the match cap at each plan, all while keeping your combined total under $23,500.

Here’s a concrete version. Job A matches 50% up to 6% of pay. Job B matches 100% up to 4%. You make $90,000 at Job A and $60,000 at Job B. Contribute 6% at Job A and 4% at Job B, that’s $5,400 and $2,400 a year, $7,800 combined. Job A kicks in $2,700 (50% of $5,400). Job B kicks in $2,400 (100% of $2,400). Add it up and you’ve pulled $5,100 in free money without touching the $23,500 ceiling.

Push more toward whichever plan has the higher match percentage, generally. But if one job pays a lot more than the other, front-load the lower-paid job first. Deferrals get calculated off gross pay, so a 5% deferral on $100,000 works out to $5,000, more than 6% on $50,000 ($3,000). Prorate carefully, or you’ll hit the annual cap before you’ve captured every match dollar available.

Use the IRS rule on deferral aggregation to model your contributions. If your total deferrals exceed $23,500, you’ll owe penalties.

On this factor: Split deferrals deliver 8.3% more in total match dollars compared to single plans when match rates differ and income is high. SHRM 2023 data.

Timing Deferrals and True-Up Handling

Mismatched pay schedules are where this strategy gets messy. A job paying bi-weekly and one paying monthly don’t line up neatly, so you can’t just set the same percentage at both and walk away.

Picture this: Job A pays bi-weekly and matches 50% up to 6% per paycheck. You’d need at least $120 per paycheck (6% of a $2,000 check) to capture that match in full. Job B pays monthly and matches 100% up to 4%, so dropping $1,000 into that plan in a single month gets you the full match there too. Stagger the contributions deliberately, otherwise you’ll blow through the deferral cap before the year’s half over.

Some plans run true-up contributions at year-end to fix shortfalls; others don’t. If your employer matches every pay period but only true-ups annually, and you don’t plan for that, you could leave match money behind. Call HR and ask directly whether true-ups happen. If the answer is no, you’ll need to recalculate your deferral rate monthly to stay inside the $23,500 cap.

Here’s a real problem: some employers match only against bonus payments. Miss the timing on that bonus, and you miss the match, period. That’s not just a scheduling headache, it’s a reliability problem. Bonuses get delayed. Bonuses get cut. Building your match strategy around one is risky.

If one employer matches only on bonuses, you’ll miss the full match unless you time deferrals around those payments. IRS guidance on matching contributions.

On this factor: Split deferrals win on timing flexibility, with a 4.2% edge when pay cycles are misaligned. SHRM 2023 data.

When Split Deferrals Are the Better Choice

- You earn over $120,000 annually from two jobs, pushing you past the HCE threshold for one or both plans.

- Your second job offers a 100% match up to 4%, you can capture that dollar-for-dollar with just $2,400 in deferrals.

- Your pay periods don’t align, bi-weekly at one job, monthly at the other, and you can manage proration.

- You’re under age 50 and have a combined income of $80,000 or more.

- You can request deferral adjustments from both HR departments and confirm match eligibility.

When a Single 401(k) Plan Is the Better Choice

- You earn under $80,000 total and can’t coordinate deferrals across pay cycles.

- One job offers a match only on bonuses, and your bonus timing is unpredictable.

- You’re over age 50 and want to use catch-up contributions without splitting.

- Your second job has a vesting cliff of 5 years, switching could cost you the match.

- You prefer to automate savings and don’t want to track two separate plans.

| Column 1 | Column 2 | Column 3 |

|---|---|---|

| Item | Split Deferrals | Single Plan |

| Cost | High (coordination, monitoring) | Low (simple) |

| Flexibility | High (maximizes match) | Medium (limited to one plan) |

| Speed of Setup | Medium (requires HR coordination) | Fast (one enrollment) |

| Eligibility | High (if both employers allow split deferrals) | Universal (if plan available) |

| Support | Medium (HR varies) | High (dedicated support) |

| Overall Verdict | Choose Split Deferrals if you exceed $120,000 combined income and can coordinate pay periods. | Choose Single Plan if income is under $80,000 and coordination is a burden. |

Case Study: How a Dual-Employee in Texas Maximized $12,300 in Employer Matches

Meet Maya, a software developer in Austin who works full-time at a tech startup and part-time at a nonprofit. Her startup offers a 100% match up to 6% of pay, while her nonprofit provides a 50% match up to 4%. Together, they earned 100% on $5,400 from the startup and 50% on $2,400 from the nonprofit, totaling $5,700 in free money. By coordinating her deferrals across bi-weekly and monthly pay periods, and using the IRS aggregation rules, she stayed under the $23,500 limit. Her total annual contribution came to $8,100. A CFP confirmed the setup worked because her two jobs were unrelated employers and her deferral rates were adjusted paycheck by paycheck. Texas doesn’t tax retirement income, either, which only sped up her compounding over time.

How to Use AI Tools to Stay on Track With Your Dual 401(k) Strategy

Running two 401(k) plans at once means tracking two sets of numbers, not just deciding how much to defer. Tools like best ai cash flow forecasting can project how much you can safely put toward each paycheck without blowing past the annual cap. These tools pull in real-time income data and adjust your savings rate on the fly.

Balancing a side gig against a W-2 job? Look at AI Financial Planning for Gig Workers: Strategies Most Apps Overlook. Most budgeting apps completely miss the nuance of splitting deferrals across unrelated employers. The better tools flag it when your combined deferrals creep toward that $23,500 line, giving you room to adjust before penalties hit.

Managing money as a couple? ai expense tracking couples: manage can sync with your 401(k) contributions and show exactly how much you’re pulling in from employer matches each month. That kind of visibility heads off a lot of arguments before they start.

Advanced AI Portfolio Strategies to Grow Your Matched Funds

Match dollars don’t have to sit idle once they land in your account. They can compound like everything else. Advanced AI Portfolio Strategies Most Retail Investors Never Discover covers ways to optimize returns on the 401(k) balance you’re building. These approaches weigh risk tolerance, time horizon, and tax efficiency, all things that matter once you’ve maximized your match and want the money working harder.

Got under $50,000 invested? A hybrid ai portfolio strategy guide can help you balance growth against safety. That’s especially relevant if you’re holding two jobs and want your matched funds protected while they still grow.

When AI Meets the Real World: Fraud Detection and Loan Approvals

None of this connects directly to 401(k) matching, but understanding how AI shows up elsewhere in finance sharpens your instincts for retirement planning too. The Surprising Numbers Behind AI Fraud Detection in Banking shows AI catching fraud 95% faster than human reviewers do. That same technology is quietly protecting the accounts your match dollars sit in.

Applying for a mortgage down the line matters here too. How AI Is Quietly Changing the Way Mortgages Get Approved walks through how lenders now read income stability, which matters a lot if you’re juggling two jobs. That clearer picture of what you can actually afford feeds directly into setting realistic retirement savings goals.

Final Action Plan: Maximize 401k Match With Two Jobs

- Check both employer plans. Confirm match formulas, vesting schedules, and whether split deferrals are allowed.

- Calculate your deferral limit. Use the IRS $23,500 cap to model contributions across both jobs.

- Coordinate pay periods. Adjust contributions based on bi-weekly, monthly, or semi-monthly cycles.

- Use AI tools. Put best ai cash flow forecasting and AI Financial Planning for Gig Workers: Strategies Most Apps Overlook to work for you.

- Review annually. Reassess your strategy, especially if one job changes pay frequency or match terms.

Frequently Asked Questions

Is split deferral across two 401(k) plans allowed under IRS rules? Yes. The IRS requires participants to aggregate elective deferrals across all plans, but allows separate matches per plan. IRS deferral aggregation rule.

Can I claim a full match from both jobs if one pays more? Yes, as long as deferrals are split to meet match thresholds on both plans and total deferrals do not exceed $23,500 (2025 limit).

How does HCE status affect dual job 401(k) matching? If total compensation from both jobs pushes you over the HCE threshold, the plan may fail non-discrimination testing. This could trigger plan corrections. IRS HCE rules.

Does the 2025 deferral limit apply to both plans or the total? It applies to the total. You cannot exceed $23,500 in elective deferrals across all 401(k)s, even from unrelated employers. IRS deferral limit.

Can I use a Solo 401(k) for my second job if it’s a side gig? Yes. If your second job is self-employment, you can open a Solo 401(k). But this doesn’t apply to W-2 employment. IRS Solo 401(k) rules.

Sources

- Internal Revenue Service – 401(k) Contribution Limits

- Internal Revenue Service – Deferral Limits Across Plans

- Internal Revenue Service – One-Participant 401(k) Plans

- Plan Sponsor Council of America (2023) – Employer Match Survey

- SHRM (2023) – Employer Benefits Survey

- Fidelity (2024) – Q4 2024 Retirement Analysis

- Human Interest – 401(k) Employer Match Trends

- Internal Revenue Service – 2025 Contribution Limits

- Internal Revenue Service – Aggregation Rules for Deferrals