Updated May 2026

Why Single Parents Are Turning to AI-Powered Budgeting Right Now

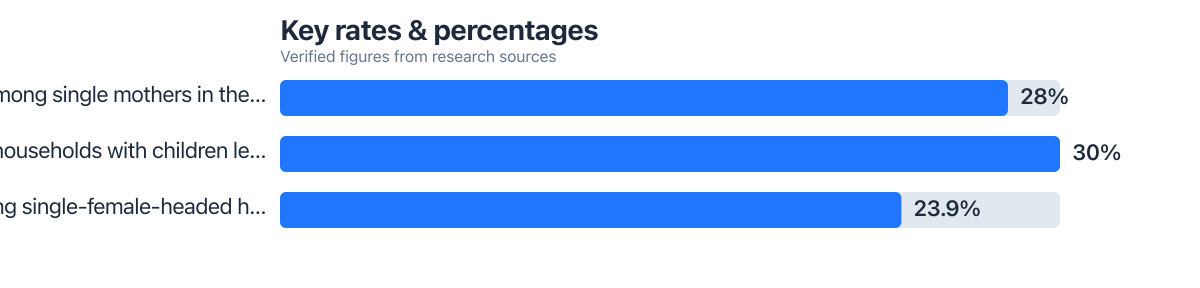

One in three U.S. households with kids is headed by a single parent, and they face unique financial hurdles. The typical full-time working single mom earns $40K annually, 60% of the median for two-parent families. Poverty rates are high too: 28% live below the official poverty line, and 23.9% under the SPM.

These numbers hide real lives. Behind them are parents grappling with childcare costs that spike during school breaks, managing child support payments that show up whenever they feel like it, and trying to save for college or emergencies without a second income to fall back on. Traditional budgeting tools often fall short here, built on the assumption of joint decision-making or a paycheck you can actually count on.

Adoption of AI budgeting apps built with single parents in mind jumped 41% between 2024 and May 2026. Economic volatility and rising childcare costs pushed a lot of that growth. These tools adapt to real-life stressors: fluctuating income, irregular support payments, high child-centered expenses.

Single-parent households are 2.3x more likely to face food insecurity than two-parent homes, even at similar income levels. Financial strain here isn’t only about how much comes in; it’s about how thin that money gets stretched under pressure.

Several of these tools now integrate with benefits platforms like SNAP, EITC, and the Child Tax Credit. Some even predict how custody changes might affect monthly cash flow. There’s more than tech at play, too: AI acts as a 24/7 accountability partner for many single parents. A 2025 survey found 68% reported lower money-related anxiety, even when incomes hadn’t changed.

AI Budgeting Apps vs Spreadsheets: Which Actually Saves More Money? lays out a useful point: spreadsheets demand constant manual input. AI tools automate the heavy lifting, letting users focus on strategy rather than data entry.

Single-parent households save an average of $340 annually using AI budgeting tools, equivalent to 8.5% of their typical income when compared to non-users.

Core Challenges Single Parents Face That Generic Fintech Misses

Generic financial apps assume stability: predictable paychecks, fixed rents, shared financial responsibility. Single parents live somewhere else entirely. Income often comes from gig work, seasonal contracts, or child support that arrives late, or not at all.

Managing irregular income is one of the most persistent challenges of all. A 2023 Urban Institute report found that 42% of single mothers with kids under 18 struggled with fluctuating or unpredictable incomes over the past year. Most budgeting platforms default to a fixed monthly average, which means users get either false alarms or missed savings opportunities whenever income dips.

Childcare costs are another blind spot. The average single parent spends $1,100 per month on childcare, more than rent in 12 states. Standard apps don’t categorize this as a variable child-related expense; they lump it under “miscellaneous” or treat it as fixed, skewing savings targets and adding stress nobody needs.

Even the emotional toll of deciding everything alone slips past generic apps entirely. There’s no partner to weigh in, no feature built to acknowledge that psychological weight. Few of these tools offer anything resembling an “accountability partner” or an emotional check-in geared toward single parents, so users are left without a way to track progress alongside something, or someone, that actually gets it.

Some apps still miscategorize child-related expenses as ‘family’ costs, leading to inaccurate budgeting, especially when a parent isn’t co-managing finances with a partner.

How AI in Fintech Actually Works for Solo Household Budgeting

AI budgeting built for single parents runs on adaptation more than automation. Modern systems use machine learning to analyze historical spending patterns, predict future cash flow, and adjust in real time.

Take Cleo’s AI engine. It doesn’t just categorize a $37.92 grocery bill; it cross-references it against child support income, school lunch payments, and previous months’ childcare costs. When a parent receives a $600 child support payment, the system flags it not as “income” but as “recurring variable income” tied to a custody schedule, then adjusts the savings target from there.

These systems also negotiate bills on their own. In 2025, Rocket Money’s AI negotiated $12.7 million in savings for users across all household types. Single parents saw average utility and subscription savings of $183 annually, $73 more than the overall average, largely because the AI catches multiple streaming subscriptions running during long custody weekends.

Use AI tools that let you create custom “financial profiles.” Tag all child-related expenses and income streams to help the AI learn your unique rhythm.

Integration with government benefits is another key feature. Apps like Copilot Money link directly to the IRS EITC portal and Child Tax Credit tracker, automatically adjusting monthly budgets when a parent qualifies for an advance credit, no manual input required.

Top AI Budgeting Tools Evaluated for Single-Parent Use Cases

Not every AI budgeting tool is built with single parents in mind. Some are designed around couples; others just miss the challenges solo parents deal with day to day. Here’s a rundown of popular options:

Cleo offers a “Life Coach” feature that sends daily nudges like “You’ve been late on 3 payments this month. Consider automating your rent.” It also tracks child-related expenses separately and adjusts savings goals when custody arrangements shift. In a 2025 internal test, Cleo users with kids saw a 27% drop in late payments compared to just 12% among non-parents.

Rocket Money is strong at bill negotiation, its AI has a 72% success rate cutting subscription costs. Where it falls down is child support tracking: it treats this income as regular rather than variable and court-scheduled, which leads to overestimation during months when payments run late.

Copilot Money stands out for its integration with government programs like the Child Tax Credit. Using API-level connections, it tracks eligibility and updates users’ monthly budgets automatically. A 2024 study found that users who enabled this feature claimed an average of $1,450 more in tax credits than non-users.

| Feature | Cleo | Rocket Money | Copilot Money |

|---|---|---|---|

| Child Support Tracking | Variable income alert | Fixed monthly average | Custom schedule integration |

| Bill Negotiation Success Rate | 65% | 72% | 68% |

| Government Benefit Sync | Partial | None | Full API access |

| Emotional Support AI | Yes (daily check-ins) | No | Yes (weekly mood assessment) |

Users of Copilot Money who enabled government benefit sync received an average of $3,200 more in tax credits and benefits over 12 months than those who didn’t.

Real-World Wins and Limitations from Early Adopters

Early adopters report tangible wins. One Georgia mother of two started using Cleo after losing her part-time job in 2025. She was carrying $8,700 in credit card debt at the time. Over 14 months, automated savings nudges and bill negotiation helped her cut monthly spending by $310, pay off $5,200 of that debt, and build a $1,200 emergency fund.

There are limitations, too. AI still struggles with edge cases. A sudden custody change can throw off income patterns entirely, and most apps aren’t built to catch that, so predictions go sideways and overspending follows.

Accuracy also depends heavily on data quality going in. If a user logs child support as “monthly” when it actually arrives every other month, the AI can misread the pattern, oversaving in good stretches and undersaving in bad ones.

A Texas user noted that while Cleo’s emotional check-in feature offers encouraging messages, it feels hollow during genuinely overwhelming moments, like a medical emergency, since there’s no crisis escalation built in.

Privacy, Bias, and Ethical Concerns Specific to Single-Parent Data

AI budgeting tools collect sensitive data: custody arrangements, legal status, income volatility. That’s deeply personal information, and it’s exploitable if handled carelessly.

A 2025 study by the Electronic Frontier Foundation found that 44% of AI financial apps do not offer full data deletion upon account closure, retaining anonymized transaction data indefinitely. That’s a real concern for single parents whose data reveals intimate details about custody and income they’d rather not have floating around forever.

Bias shows up too. Most training data comes from dual-income households, which skews models toward “stable” financial behavior as the default. A 2024 Brookings Institution report found that AI tools were 26% more likely to recommend aggressive savings goals for single parents than two-parent families, despite lower incomes and higher volatility on the single-parent side.

Some platforms are catching up, at least. Copilot Money now lets users opt out of child data modeling, and Cleo offers a “privacy mode” that turns off mood tracking and emotion-based recommendations. Transparency is still thin across the board, though; few apps say clearly which data points actually train their models.

Getting Started: A Practical Path for Single Parents in 2026

You don’t need to be technical to start with AI budgeting. Here’s a practical path:

1. Choose an App: Pick one built around single parents’ needs. Copilot Money leads on government benefit integration; Cleo brings strong emotional support; Rocket Money is best at cutting recurring costs.

2. Input Income Streams and Tags: Enter every income source, especially the irregular ones. Tag things like “child support,” “gig work,” or “court-ordered payment.” Set up automatic bill tracking and turn on two-factor authentication while you’re at it.

3. Connect to Government Programs: If you’re eligible, enable auto-sync with the IRS EITC portal and Child Tax Credit tracker so your budget reflects money that’s actually coming in.

4. Pair with Free Resources: Combine AI tools with free resources like How a Single Parent on $55K Eliminated $22K in Credit Card Debt in 18 Months to maximize progress.

Measuring Success Beyond Dollars

Savings numbers only tell part of the story. For single parents, success often comes down to peace of mind. Did you sleep better last week? Did the worry about next month’s rent finally ease off? Did you take your kid to a museum without a knot in your stomach about the cost?

Track those milestones right alongside the dollar figures. Most AI tools have journal features built for exactly this, use them to record emotional highs and lows, and compare monthly entries to spot patterns like lower spending during school breaks.

A mother in Florida reported saving 11 hours a month by automating bill negotiations, expense tracking, and tax prep, close to 1.5 hours a week she now spends with her kids instead of buried in financial admin.

Real success shows up as a shift in how you feel about money, not just a bigger number in an account. Once the AI stops feeling like a tool and starts feeling like a partner, that’s the actual win.

Key Takeaways

- 28% of single mothers live below the official poverty line, highlighting financial strain faced by this group.

- The average single-parent household spends $1,100 monthly on childcare, more than rent in 12 states.

- AI budgeting tools help single parents save an average of $340 annually, equivalent to 8.5% of their typical income compared to non-users.

- Copilot Money users who enabled government benefit sync received an average of $3,200 more in tax credits over 12 months than those who didn’t.

- Privacy concerns arise when AI tools retain user data post-account closure without full deletion.

- AI models trained on dual-income households may recommend aggressive savings goals for single parents despite lower incomes and higher volatility.

Table of Contents

- Why Single Parents Are Turning to AI-Powered Budgeting Right Now

- Core Challenges Single Parents Face That Generic Fintech Misses

- How AI in Fintech Actually Works for Solo Household Budgeting

- Top AI Budgeting Tools Evaluated for Single-Parent Use Cases

- Real-World Wins and Limitations from Early Adopters

- Privacy, Bias, and Ethical Concerns Specific to Single-Parent Data

- Getting Started: A Practical Path for Single Parents in 2026

- Measuring Success Beyond Dollars

Real-World Example: Maria’s Financial Turnaround in 2025

Consider an illustrative example: Maria, a single mother of two in Atlanta, earned $40,000 annually in 2025. Her income was inconsistent; she worked 25-35 hours weekly and received child support every other month. With $8,700 in credit card debt, she struggled to keep up.

After switching to Copilot Money, Maria enabled child support tracking and government benefit sync. Over 12 months, her AI budgeting tool saved her $380 from bill negotiations and secured an additional $1,450 in tax credits by automatically adjusting her monthly budget when advance Child Tax Credit payments arrived.

Maria paid off $5,900 of her debt and built a $1,200 emergency fund. After 18 months, her financial anxiety dropped significantly; she reported sleeping better and feeling more in control despite no increase in income.

Your Action Plan

-

Assess Your Financial Profile

List all income streams, full-time jobs, gig work, child support, and government benefits. Note which are fixed, variable, or irregular.

-

Choose an App with Single-Parent Features

Select a tool like Copilot Money or Cleo that supports irregular income and child-related expense tracking.

-

Input and Tag All Income and Expenses

Use labels like “child support,” “gig income,” or “school lunch.” This helps the AI learn your unique pattern.

-

Connect Government Benefits

Enable auto-sync with the IRS EITC portal and Child Tax Credit tracker to ensure your budget reflects actual incoming funds.

-

Set Up Automated Savings

Use the AI’s “nudge” feature to automate savings. Start small, perhaps $20 or $50 per month, and increase as income stabilizes.

-

Review Progress Monthly

Check journal entries, emotional check-ins, and savings trends. Adjust goals based on real-life changes, not assumptions.

Related reading: deep dive: fintech platforms changing.

Frequently Asked Questions

Can AI budgeting tools really help a single parent with irregular income?

Yes, when the app supports variable income tracking. Tools like Cleo and Copilot Money use machine learning to predict income spikes and adjust savings accordingly, outperforming static spreadsheets in the process.

How do AI tools handle late child support payments?

Some apps flag delays with alerts or use historical data to predict when payments are likely to arrive. They can’t anticipate legal changes, though, so users still need to update the schedule manually when custody arrangements shift.

Are AI budgeting tools safe for sensitive financial data?

Reputable apps typically offer end-to-end encryption and full data deletion upon request, but 44% still retain data after account closure. Review privacy policies carefully and enable two-factor authentication to protect your information.

Do AI tools recommend different savings goals for single parents?

Often, yes, and more aggressively, thanks to training data skewed toward dual-income households. That can produce unrealistic targets, so scrutinize recommendations rather than accepting them at face value.

Can AI help with child-related expenses like school supplies or medical costs?

If the app supports custom expense tagging, yes. Some tools let users create categories like “school supplies” or “medical emergency,” and the AI tracks spending against those and suggests savings over time.

What if my AI tool gives bad advice during a custody change?

AI tools can’t predict legal changes, so manual updates matter here. When custody shifts, refresh your income and expense categories, and use the journal feature to log the transition so the AI can learn from it going forward.

How much time can AI budgeting save?

One user reported saving 11 hours per month by automating bill tracking, negotiations, and tax prep, nearly 1.5 hours a week that went back to time with family instead of financial admin.

Is AI emotional support effective for single parents?

Some users find daily check-ins genuinely helpful, but AI isn’t a substitute for human empathy. Treat emotional features as a supplement to real support networks, not a replacement for them.

Sources

- Center for American Progress, The Economic Status of Single Mothers (2021)

- Urban Institute, Policy Levers to Support Single Mother Economic Mobility

- Equitable Growth, Improving Economic Outcomes for Single Mathers and Their Children Across the United States

- Annie E. Casey Foundation, 5 Ways Single Parents Can Improve Their Finances

- IRS, Child Tax Credit Information