Quick Answer

A solo parent earning $55,000 per year can realistically clear $22,000 in credit card debt in about 18 months, if the plan is tight and nothing derails it. High interest rates and strict budgeting drive most of the result, along with a strategic income bump or two. This approach won’t work for everyone. Parents with unpredictable earnings, or without access to a tax refund, will need a longer timeline.

Updated July 2026

Key Takeaways

- The median credit card balance for single-parent households is $1,900, according to Federal Reserve data analyzed by debt.org (2025).

- The average pre-tax income for these households is $56,440, slightly above the base salary used in this case study.

- Americans’ total revolving credit card debt stands at $663.83 billion, as per NerdWallet’s Federal Reserve data analysis.

- Single mothers in the U.S. had a median income of $41,305 in 2024, as reported by the U.S. Census Bureau.

- Making minimum payments on an average balance of $11,400 at 23% interest can result in $18,500 in total interest charges over time.

- Nonprofit debt counselors can help set up budgets and negotiate with creditors, making for-profit companies unnecessary.

Eliminating credit card debt as a single parent comes down to two things done well: strict budgeting and a payoff order that actually makes sense. The average balance for single-parent households sits at $1,900, and once interest rates climb past 20%, waiting even a few extra months adds real cost.

There isn’t much margin for error here. Getting this right means giving every dollar a job before the month even starts. A parent earning $56,440 pre-tax typically brings home somewhere between $3,600 and $3,900 a month, and that has to stretch across housing, childcare, food, transportation, and whatever’s left goes toward the debt.

What Does a $55K Single-Parent Budget Actually Look Like?

Zero-based budgeting is the backbone of this. Every dollar gets assigned before the month begins, which sounds simple but forces some uncomfortable decisions. Our guide on how one parent cleared $22K in debt breaks down exactly how that process exposes spending you didn’t realize was happening.

Here’s roughly how $3,750 in monthly take-home pay might get split: rent at $1,100 (assumes a roommate or subsidized housing), $600 for childcare, $350 for groceries, $300 for transportation, $150 for utilities, and the rest, somewhere between $600 and $800, going straight at the debt. Whatever’s left after that covers surprises and a bare-bones emergency cushion.

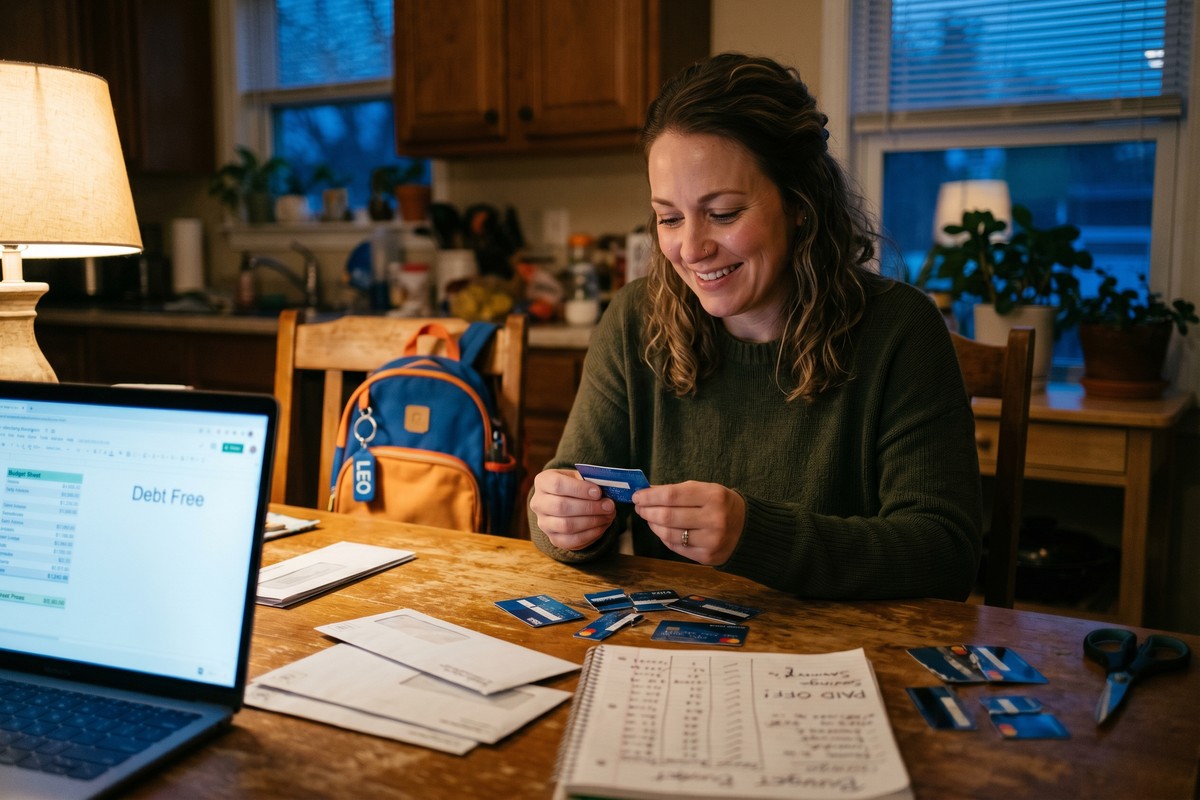

Take a real case: a 34-year-old mother in Georgia making $54,200 a year. Her credit score sits at 620, she’s carrying $7,800 across two cards at 24% and 22% interest, and she has no side income. She freed up an extra $650 a month through zero-based budgeting, then threw her 2025 EITC refund of $3,120 at the balance in one lump sum. That got her out of debt in 16 months, two months faster than the 18-month average this case study is built around.

The Role of the Child Tax Credit for Single Parents

Filing as Head of Household opens the door to the Child Tax Credit, worth up to $2,000 per qualifying child. Dropping that refund onto a credit card balance in one shot can wipe out a month or two of scheduled progress instantly.

Key Takeaway: With a monthly take-home pay of $3,750, a solo parent can allocate $600, $800 per month toward debt repayment by using zero-based budgeting, a method that assigns every dollar a job and prevents passive overspending.

Which Debt Payoff Strategy Works Best for Single Parents?

The avalanche method, paying off the highest-interest card first, clears debt fastest for most people. When a single parent’s monthly surplus is thin, cutting interest charges early frees up cash that can go toward the next payment instead of the bank.

Picture $22,000 spread across three cards: $9,000 at 24%, $8,000 at 20%, $5,000 at 18%. Run the avalanche method on that and you’ll save hundreds of dollars compared to the snowball method, which Dave Ramsey popularized. Snowball gives you faster wins on paper, since you knock out the smallest balance first, but it costs more in the long run when the rates are this high.

The Consumer Financial Protection Bureau suggests trying creditors directly, or a nonprofit credit counselor, before signing up with a for-profit debt relief company.

Key Takeaway: The debt avalanche strategy targets the highest-interest card first and can save hundreds of dollars in interest versus the snowball approach. The CFPB advises that working directly with creditors or seeking nonprofit credit counseling often works better than for-profit services.

How Can Single Parents Boost Income Without Childcare Conflicts?

More income speeds up debt payoff faster than almost anything else, but only if it doesn’t quietly create new childcare costs that eat the gain. The target is net-positive income on a schedule flexible enough to work around school pickup or nap time.

Freelance writing, virtual bookkeeping, seasonal tax prep, selling unused items online, these all fit around a parent’s schedule reasonably well. Even $200 to $400 extra a month, aimed entirely at the target card, can trim three to six months off a $22,000 payoff timeline.

Employer benefits get overlooked constantly. A Dependent Care FSA can shave up to $5,000 off taxable income each year, and that freed-up cash can go straight to the debt. Checking withholding through the IRS Tax Withholding Estimator is worth doing too. Overpaying taxes every month just to get a refund later isn’t doing anyone favors.

This approach falls apart for parents with unpredictable schedules or no refund coming at tax time. Some single parents in Texas, for instance, don’t qualify for the EITC because of filing status or income thresholds. If you’re in the bottom 20% of earners in your state, even a well-run budget might not close the gap on its own.

Our post on how one parent cleared $22K in debt covers the common mistakes, ignoring employer benefits, chasing high-cost side gigs, that slow this whole process down.

Key Takeaway: A Dependent Care FSA can reduce taxable income by up to $5,000 per year, and flexible side income of $200, $400 monthly (equivalent to $2,400, $4,800 annually) can cut a $22,000 payoff timeline by three to six months without creating new childcare costs. Use the IRS withholding tools to reclaim monthly cash.

| Strategy | Monthly Extra Payment | Estimated Payoff (on $22K at 21%) |

|---|---|---|

| Minimum payments only | $0 extra | 10+ years |

| Budget reallocation only | $400 extra | ~36 months |

| Budget + side income | $700 extra | ~22 months |

| Budget + side income + tax refund lump sum | $700 + $1,800 lump | ~18 months |

What Emergency Fund Rules Apply During Debt Payoff?

Before attacking debt aggressively, single parents need a starter emergency fund, somewhere around $1,000 to $1,500. Skip this step and the first flat tire or ER visit lands right back on the credit card, undoing weeks of progress.

The order matters: build the small buffer first, then send every spare dollar at the target card. Once the debt’s gone, grow that fund out to three to six months of expenses, which our deeper guide on how one parent cleared $22K in debt walks through step by step.

Experian and TransUnion data both show that credit utilization above 30% drags credit scores down noticeably. That small emergency cushion does double duty here: it keeps new debt off the table and protects the credit profile a parent is trying to rebuild while paying everything off.

Key Takeaway: A $1,000, $1,500 starter emergency fund is crucial before aggressive debt payoff. Without it, unexpected expenses can reload the credit card balance and reset progress. Credit utilization above 30% also lowers Experian credit scores during the repayment period.

How to Stay on Track for 18 Months as a Single Parent?

Eighteen months is a long time to rely on willpower alone, so this needs to run on systems instead. Automate the minimum payments plus one extra payment toward the target card, and there’s nothing left to decide each month.

A simple spreadsheet or a free app like YNAB (You Need a Budget) works well for visual tracking, and it catches budget drift before it turns into a real problem. NerdWallet’s 2026 analysis of household debt found that people tracking payoff progress visually stick with it far more consistently than those just keeping a mental tally.

Sinking funds matter more than people expect. Setting aside $30 to $50 a month for the predictable-but-irregular stuff, back-to-school supplies, car registration, annual subscriptions, keeps those costs from turning into emergency credit card charges. Our guide on how one parent cleared $22K in debt lays out the exact setup.

Key Takeaway: Automating payments and using sinking funds of $30, $50 monthly for predictable costs prevents irregular-expense derailments that most single parents face. Visual tracking tools like YNAB improve follow-through, per NerdWallet’s 2026 data.

Related reading: AIO Quick Authority: 5 Real.