Updated April 2026

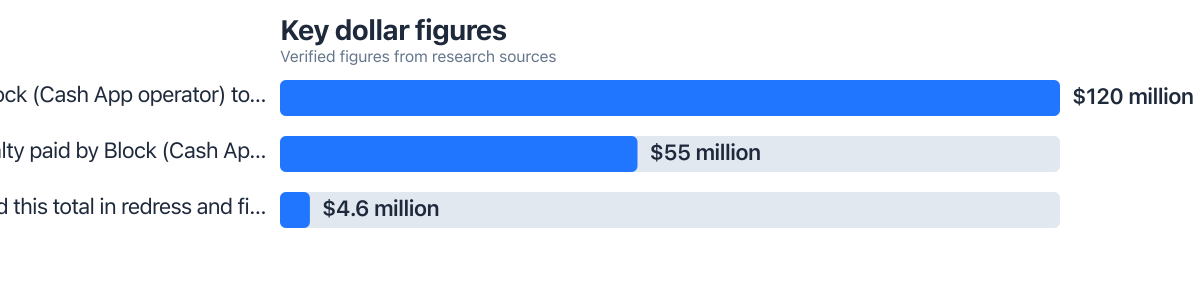

Here’s what the data shows: the Consumer Financial Protection Bureau ordered Block, the operator of Cash App, to pay up to $120 million in refunds and redress to consumers harmed by failures to investigate unauthorized transactions and issue timely refunds, plus a separate $55 million civil penalty on top of that, according to the CFPB’s 2025 order. That single enforcement action tells you something the marketing pages of most instant refund apps never mention: the promise of a fast refund and the reality of getting one are not always the same thing.

Today, a growing list of fintech apps, from PayPal and Cash App to Revolut and a handful of neobanks riding SEPA Instant rails, advertise instant or same-day refunds on returns, cancellations, and disputed charges. Some deliver exactly what they claim. Others gate the “instant” label behind verification tiers, daily caps, and fine print that most users never read.

The scope of the problem is bigger than one company. A separate enforcement case against a fintech firm resulted in $4.6 million in combined redress and fines for allegedly withholding account-closure refunds beyond the 14-day window it had promised customers, according to Hudson Cook’s 2024 enforcement summary. Meanwhile, merchants absorbing the cost of these speedier refund promises reported a 30 percent jump in chargeback-related losses in 2023 versus 2022, according to the LexisNexis True Cost of Fraud data cited in a 2025 Federal Reserve note on pay-by-bank use cases. That’s not a rounding error. It’s a sign that “instant” comes with real financial exposure somewhere in the chain, even when it’s invisible to the person tapping “confirm return.”

This guide breaks down which instant refund apps actually deliver on their promise in 2026, how the underlying payment rails make same-day credits possible, where the dollar caps and verification hurdles sit, and when waiting for a standard refund is the smarter move. You’ll come away knowing exactly which platforms to trust for which situations, what fees or limits to expect, and how to protect yourself if an instant credit gets clawed back later.

Key Takeaways

- The CFPB ordered Cash App’s operator to pay up to $120 million in consumer redress plus a $55 million penalty for fraud-refund failures, per its 2025 enforcement action.

- Revolut caps instant refund transfers at €1,000 per transaction before requiring extra verification, according to its 2025 policy documentation.

- Merchants saw a 30 percent year-over-year increase in chargeback losses in 2023, a cost that indirectly funds faster refund features.

- A separate fintech firm paid $4.6 million in fines and redress for withholding refunds beyond a promised 14-day window.

- Cash App restricts instant Cash Card credits to identity-verified users within daily limits tied to account history.

- FedNow and RTP rail adoption since 2023 has cut the technical bottleneck for real-time refund settlement, though internal risk holds still apply.

In This Guide

- What Instant Refunds Actually Mean in 2026 Fintech

- Apps Currently Advertising True Instant Refunds

- How the Technology Delivers Same-Day or Real-Time Credits

- User Experience: Speed, Limits, and Friction Points

- Fees, Limits, and Hidden Costs Compared

- Security, Fraud, and the Regulatory Landscape

- Dedicated Refund Apps: Refundid, Reshop, and the Field

- Edge Cases That Trip Up Instant Refund Users

- Who Benefits Most and When to Avoid Instant Refunds

- Is the Refund-First Model Sustainable

What Instant Refunds Actually Mean in 2026 Fintech

An instant refund app is a payment platform or third-party service that credits money back to a user within minutes or hours instead of the traditional three-to-ten business day wait tied to card network settlement. That’s the plain definition. What it means in practice varies wildly by provider, and the gap between marketing copy and actual delivery is where most user complaints originate.

Traditional refund timelines exist because of how card networks like Visa and Mastercard batch and settle transactions; a merchant issues a refund, the acquiring bank processes it, the card network routes it, and the issuing bank posts it to your account. That chain can take a week or more. Instant refund apps short-circuit part of this by crediting an internal wallet balance immediately, then settling the underlying transaction on their own timeline behind the scenes.

The feature became a genuine competitive differentiator after 2025, when several major platforms, including neobanks like SoFi and Chime, started advertising instant refunds as a retention tool rather than a niche perk. Fintechs realized that speed of refund correlates strongly with user trust, especially among people who’ve been burned by slow processing at traditional banks like Chase or Bank of America. It’s a cheap way to win loyalty, provided the risk engine behind it doesn’t blow up in fraud losses.

There’s an important distinction between consumer-facing refund features and the B2B payment rails that make them possible. Apps like PayPal or Cash App give an end user the appearance of instant money, but underneath, they’re often relying on internal ledger credits rather than actual bank-to-bank settlement. True instant settlement, where money moves between financial institutions in real time, depends on infrastructure like the Federal Reserve’s FedNow service and The Clearing House’s RTP network in the U.S., or SEPA Instant in the EU.

That distinction matters because it determines what happens if something goes wrong. An internal ledger credit can be reversed by the platform with a few lines of code; a real interbank transfer settled through FedNow is much harder to claw back once it lands.

Instant Refunds vs. Instant Transfers: Not the Same Thing

Many users conflate “instant refund” with “instant transfer,” but they solve different problems. An instant refund credits your in-app balance or card immediately after a return or cancellation is approved. An instant transfer moves that balance out to your external bank account, usually for a small fee. Confusing the two is the single biggest source of user frustration in app store reviews from late 2025 onward.

Apps Currently Advertising True Instant Refunds

As of early 2026, three consumer-facing platforms dominate the conversation around instant refunds: PayPal, Cash App, and Revolut. Each has a documented, publicly stated policy, though the fine print differs enough that treating them as interchangeable is a mistake.

PayPal’s own documentation states that eligible goods purchases receive instant refunds to a user’s PayPal balance in supported markets, a policy formalized in its 2025 terms update.

PayPal’s approach is the most mature of the three. Refunds for eligible purchases land in a user’s PayPal balance almost immediately rather than routing back through the original card or bank, which sidesteps the multi-day card network delay entirely. The catch is that “eligible” excludes a meaningful slice of transactions, particularly those funded by credit card rather than balance or linked bank account.

Revolut takes a more tiered approach. Its instant transfer feature for refunds caps out at €1,000 per transaction, with additional identity verification required above that threshold, according to the company’s 2025 policy pages. That cap is rarely advertised prominently, which means users initiating a large refund often hit a wall they didn’t expect, triggering document uploads and a delay that undercuts the entire “instant” pitch.

Cash App’s refund policy is the strictest of the three. Instant credits to a linked Cash Card are available only after identity verification, and even then, daily limits apply based on account history and usage patterns, per its terms of service. New or lightly used accounts see much lower ceilings than accounts with a longer transaction history. Given the CFPB’s 2025 findings about Cash App’s fraud-investigation failures, this caution is arguably justified, even if it frustrates users expecting instant gratification.

| App | Instant Refund Cap | Verification Trigger | Settlement Method |

|---|---|---|---|

| PayPal | Varies by market; no fixed public cap for balance credits | Standard account verification | Internal balance credit |

| Revolut | €1,000 per transaction | Enhanced ID check above cap | Instant transfer via internal rails |

| Cash App | Daily limit tied to account history | Full identity verification required | Cash Card instant credit |

Beyond these three, a handful of regional players are gaining traction, particularly in the EU where SEPA Instant adoption has pushed smaller neobanks to offer comparable features. None of these newer entrants has published enforcement history or regulatory scrutiny comparable to PayPal, Cash App, or Revolut, so their track record is thinner and harder to verify independently.

How the Technology Delivers Same-Day or Real-Time Credits

The infrastructure making any of this possible is the shift toward real-time payment rails. In the U.S., the Federal Reserve’s FedNow service and The Clearing House’s RTP network allow banks to settle transactions in seconds rather than days, a change that rippled through refund processing after broader bank adoption in 2023 through 2025. In the EU, SEPA Instant plays the equivalent role.

Here’s what most coverage of these rails misses: adoption by a bank doesn’t automatically mean every fintech app built on top of it passes the speed through to refunds. A platform can be connected to FedNow for deposits while still running refunds through a legacy batch process, because refunds touch fraud-review systems that transfers don’t.

That’s where internal risk engines come in. Every instant refund app runs some form of real-time fraud scoring before releasing funds, checking transaction history, device fingerprints, and behavioral signals not unlike the models that feed a FICO Score or the fraud alerts consumers see from credit bureaus like Experian. When the risk engine flags something as suspicious, the “instant” credit either gets delayed for manual review or, in worse cases, gets issued and then reversed days later once a human investigator looks at it. Hold periods behind the scenes are the norm, not the exception, even when the front-end experience feels immediate.

The CFPB’s 2025 order against Block covers up to $120 million in consumer redress tied specifically to failures in investigating unauthorized transactions and issuing timely refunds, on top of a $55 million civil penalty.

The distinction between card network integration and bank transfer integration also shapes speed. A refund routed back to the original card typically still depends on the card network’s settlement cycle, even if the fintech itself processes instantly on its end. A refund routed through a bank transfer rail like RTP or FedNow, both of which operate under Federal Reserve and FDIC-supervised bank participation rules, can bypass that entirely, which is why apps increasingly nudge users toward linked bank accounts or in-app balances rather than card refunds.

User Experience: Speed, Limits, and Friction Points

In practice, the “instant” experience is gated behind dollar caps and verification steps that most users don’t discover until they hit them. Revolut’s €1,000 ceiling is a good example: a refund for a European vacation booking or a large electronics purchase can easily exceed that threshold, forcing a user into an identity check mid-transaction that adds friction right when speed was the entire selling point.

Mobile and desktop experiences diverged more than expected in 2025 and early 2026 reviews. Several apps process instant refund requests only through their mobile app, routing desktop or web-based requests through a slower standard queue. This isn’t always disclosed clearly, and it’s led to a pattern of confused users assuming a feature is broken rather than simply unavailable on their chosen device.

Verification steps themselves range from a quick selfie-based identity check to full document upload and manual review that can take a day or two, which defeats the purpose of an instant refund entirely. The irony isn’t lost on frustrated users: an app promoted specifically for speed can end up slower than a traditional bank refund once verification friction kicks in.

An instant refund credited to your balance isn’t guaranteed final. If a platform’s fraud review later flags the original transaction as disputed or unauthorized, it can claw back the credit days or weeks after the fact, sometimes leaving your balance negative.

Clawbacks are the most consequential friction point, and they’re poorly understood by most users. When an instant refund is later reversed, either because the original purchase gets disputed, the fraud engine flags it retroactively, or the merchant contests the return, the app typically debits the balance again. If a user has already spent or withdrawn that money, this can result in a negative balance, a blocked account, or a collections process, depending on the platform’s terms.

Fees, Limits, and Hidden Costs Compared

Speed rarely comes free, even when a platform markets the refund itself as fee-free. The direct fee schedules differ depending on whether you want the refund to stay in an app balance or move out to an external bank account, and this is where a lot of the real cost hides.

PayPal generally doesn’t charge for the initial balance credit, but moving that balance to a linked bank account instantly (versus the standard 1-3 day transfer) often carries a small percentage fee, typically in the 1-1.75% range depending on the transfer type and destination. Revolut’s instant transfers can be free for certain account tiers but tiered or capped for others, with premium plans unlocking higher limits. Cash App similarly offers a standard free transfer alongside a paid instant option, usually a flat percentage fee on the transferred amount.

Here’s a simple way to see the real cost. Say you’re owed a $500 refund and your app charges a 1.5% instant transfer fee to move it to your bank the same day, versus a free standard transfer that takes three business days. The instant option costs you $7.50 outright. But consider the opportunity cost of waiting: if that $500 would otherwise sit in a high-yield account earning roughly 4.5% APY, three days of lost interest is only about $0.19, negligible compared to the fee. In this case, paying for speed rarely makes financial sense unless you have an urgent, time-sensitive need for the cash, like an overdue bill or a rent payment due immediately.

Before paying an instant transfer fee, check whether you actually need the cash today. If not, the standard free transfer almost always beats the fee on a pure dollars-and-cents basis; the interest you’d lose by waiting is usually far smaller than the fee charged for speed.

Merchants aren’t immune from this cost structure either. When a platform enables instant refunds, someone has to front that liquidity before the underlying transaction fully settles, and merchants often absorb a portion of that risk through higher processing fees or stricter chargeback terms. The 30 percent jump in merchant chargeback losses reported in the 2024 LexisNexis data referenced by the Federal Reserve reflects part of this dynamic; faster refund promises can make disputing a fraudulent chargeback harder for merchants after the fact, since the money’s already out the door. Small business owners juggling this kind of cash-flow uncertainty often look toward tools covered in our best ai cash flow forecasting guide to model these swings ahead of time.

Security, Fraud, and the Regulatory Landscape

The regulatory backdrop for instant refunds tightened considerably heading into 2026, largely in response to enforcement actions like the one against Block. Regulators including the CFPB and, in some product categories, the FDIC, are increasingly scrutinizing not just whether refunds happen, but how quickly complaints get investigated and whether “instant” features create new fraud vectors that didn’t exist under slower, more manually reviewed systems.

Documented fraud vectors specific to instant refund features include account takeover schemes where a bad actor initiates a fraudulent return or dispute, collects the instant credit, then withdraws it before the platform’s risk engine catches up. Because the credit lands before full verification completes in many cases, this window of a few hours to a couple of days becomes the exploit target. It’s a structural weakness baked into the speed-first design.

Consumer protection differs meaningfully between markets. In the U.S., the CFPB has taken direct enforcement action tied to refund timeliness, as seen in both the Block case and the smaller $4.6 million fintech enforcement case from 2024. In the EU, PSD2 and its successor frameworks impose stricter authentication requirements on payment providers, which can slow down instant features but generally offers stronger dispute-resolution guarantees to consumers. Neither system is perfect, but the EU’s approach leans more toward mandated verification even at the cost of speed, while the U.S. approach has historically relied more on after-the-fact enforcement.

The same fraud-detection systems banks use to flag suspicious transactions in real time are increasingly the backbone of instant refund risk engines; our surprising numbers behind ai fraud piece breaks down how these models actually work behind the scenes.

Anyone relying heavily on instant refund features should treat the underlying account like any other financial account worth protecting: strong authentication, monitoring for unexpected balance changes, and understanding that a fast credit isn’t automatically a final one until the dispute window closes.

Dedicated Refund Apps: Refundid, Reshop, and the Field

Beyond general-purpose payment apps, a smaller category of dedicated refund apps has emerged specifically to solve the “instant refund before you ship the item back” problem for online shoppers. Names like Refundid, Reshop, and Fastback have built a niche business model around this exact pain point, and a side-by-side look at how they compare is useful for anyone shopping frequently online.

| Service | Model | Typical Approval Speed | Retailer Coverage |

|---|---|---|---|

| Refundid | Pays refund upfront, keeps returned item value if not shipped in window | Minutes to hours | Selected online retailers, expanding list |

| Reshop | Advance refund tied to browser extension detection of eligible returns | Same-day typical | Partner retailer network |

| Fastback | Similar advance-refund model, focused on fashion and apparel returns | Same-day to next-day | Retail partners in apparel/lifestyle categories |

These services operate on a business model that’s structurally different from PayPal, Cash App, or Revolut: they’re essentially fronting the refund themselves, betting that most users will actually ship the item back within the promised window (commonly seven to fourteen days), and recouping their exposure through partner retailer agreements or a small service fee built into the transaction. When a user doesn’t return the item in time, the service can charge the original card or deduct from a linked account, which is a risk users often don’t fully grasp until it happens to them.

None of these dedicated refund apps has published enforcement history comparable to the CFPB actions against Block or the fintech firm fined $4.6 million, which makes it harder to independently verify their fraud-loss rates or complaint volumes. That’s a meaningful gap. Without regulatory filings or third-party audits, users are largely relying on app store reviews and word of mouth to judge reliability, which is a thinner evidence base than what’s available for the major platforms.

Edge Cases That Trip Up Instant Refund Users

International shipping and returns complicate instant refunds considerably. A refund promised “instantly” domestically often reverts to standard multi-day processing once currency conversion or cross-border banking rails are involved, since FedNow, RTP, and SEPA Instant don’t interoperate across borders the way domestic transfers do. Someone returning an item bought while traveling abroad should expect the standard timeline, not the instant one, regardless of what the app’s homepage promises.

Disputed returns after an instant payout create a genuinely messy situation. If a retailer inspects a returned item and determines it’s damaged, used, or not the item originally purchased, the refund can be reversed even after the money has already been spent by the consumer. This is functionally similar to a chargeback in reverse, and consumers have far less established recourse here than they do with traditional credit card disputes.

Tax reporting is an overlooked wrinkle for frequent users, particularly anyone running a resale business or using these apps at high volume. Balance credits and instant transfers can trigger reporting thresholds under IRS rules for third-party payment platforms (Form 1099-K), and frequent instant refund activity can complicate reconciling what counts as taxable income versus a simple return of funds. Freelancers and gig workers juggling multiple payment apps for both income and refunds may find it worth reviewing strategies in our ai financial planning gig workers resource, since the recordkeeping habits that help with taxes also help catch refund discrepancies faster.

Integration failures are common enough to plan around. A refund initiated through a linked debit card can fail silently if the card has expired or been replaced, leaving the user waiting on a credit that never arrives without any clear notification of the failure. This happens often enough with dedicated refund apps tied to browser extensions that users should manually confirm receipt rather than assume silence means success.

Who Benefits Most and When to Avoid Instant Refunds

Frequent online shoppers who return items regularly, gig workers managing tight cash flow between gigs, and travelers dealing with cancelled bookings are the clearest beneficiaries of instant refund features. For these users, the difference between waiting ten days and getting money back same-day can directly affect whether a bill gets paid on time or a bank account dips into overdraft.

Gig workers in particular benefit because their income is already irregular; an instant refund on a cancelled purchase or returned item can smooth over a gap that would otherwise require dipping into savings or, worse, a high-APR credit line. Gig workers should weigh instant refund fees against their actual cash-flow need on a case-by-case basis rather than defaulting to the fastest option every time.

There are clear scenarios where waiting for standard processing is the safer, and often cheaper, choice. Large purchases above a platform’s instant cap (like Revolut’s €1,000 threshold) will trigger verification friction anyway, so there’s little upside to trying the instant route first. Business accounts handling refunds at volume should also be cautious, since instant refund features are generally built and tested around personal account use cases, not the higher transaction volumes and compliance requirements business accounts carry under bank partner agreements with institutions like Chase or regional FDIC-insured banks.

Merchants absorbing faster refund promises saw a 30 percent increase in chargeback losses in 2023 versus the prior year, according to the LexisNexis data cited by the Federal Reserve in 2025.

Anyone managing shared finances, like couples splitting expenses and refunds across accounts, may find the friction of instant refund clawbacks especially disruptive to a shared budget; the coordination tips in our ai expense tracking couples manage guide address exactly this kind of shared-account complexity.

Is the Refund-First Model Sustainable

The honest answer is that nobody fully knows yet. The refund-first model, where a platform or dedicated app fronts money before the underlying transaction is verified, works only as long as fraud and non-return rates stay within a tolerable range for the business absorbing the risk. When those rates spike, as the merchant chargeback data suggests they have, the business either tightens verification (undercutting the “instant” promise) or eats the loss.

Regulatory pressure adds another layer of uncertainty. The CFPB’s willingness to impose penalties in the hundreds of millions for refund-related failures signals that regulators view speed promises as enforceable commitments, not just marketing language. That raises the cost of getting it wrong for any fintech chasing rapid growth in this space, which may slow the pace of new entrants relative to what the 2023-2025 period saw.

Whether this model survives in its current form over the next several years likely depends on how well platforms balance genuine instant settlement (via rails like FedNow and RTP) against the fraud exposure that speed creates. For now, treat any instant refund feature as a convenience with real limits, not a guarantee, and read the verification thresholds and clawback terms before relying on it for anything financially significant.

Real-World Example: A Frequent Online Shopper Weighs Instant vs. Standard Refunds

Consider an illustrative example: a shopper who returns roughly four to five online orders per month, averaging $150 per return, decides to test whether paying for instant transfers is worth it over a full year. Using a hypothetical instant transfer fee of 1.5%, each $150 refund costs about $2.25 to receive same-day instead of waiting the standard three business days for a free transfer.

Over 12 months, assuming 54 returns total (4.5 per month), that adds up to roughly $121.50 in cumulative fees just for speed. Against that, the shopper calculates the opportunity cost of waiting: if that money would otherwise sit in a savings account earning 4.5% APY, three days of delay on $150 costs about $0.06 in lost interest per return, or roughly $3.24 across all 54 returns for the year.

Before the analysis, the shopper had been defaulting to the instant option every time, assuming it was “basically free” since the standard transfer showed up as free anyway and the instant fee felt small on any single transaction. After running the numbers, the picture changed: paying $121.50 a year to save what amounts to roughly $3.24 in foregone interest is a poor trade unless the cash is needed immediately for a specific bill or expense.

The shopper’s revised approach: use instant transfers only for the roughly 20% of returns tied to a genuinely urgent cash need, and let the rest process through the free standard timeline. That single change cut the shopper’s annual instant-transfer fees from around $121.50 down to roughly $24.30, a savings of close to $97 a year with no real downside beyond a few extra days’ wait on non-urgent refunds.

Your Action Plan

-

Check your app’s actual instant refund cap before you need it.

Look up whether your platform has a documented ceiling, like Revolut’s €1,000 threshold, so a large refund doesn’t unexpectedly stall on a verification request mid-transaction.

-

Complete identity verification proactively, not reactively.

Apps like Cash App gate instant credits behind full identity verification; finishing this step before you’re in the middle of a refund request avoids losing the speed benefit entirely.

-

Calculate the real cost of an instant transfer fee against your actual need for the cash.

As the worked example above shows, a small percentage fee on every transfer adds up fast against a comparatively tiny opportunity cost of waiting a few days; reserve instant transfers for genuine emergencies.

-

Read the clawback and dispute terms for any dedicated refund app before you use one.

Services like Refundid or Reshop front the refund and expect the item shipped back within a set window; missing that window can mean the charge comes right back to your card.

-

Keep records of every instant refund for tax season if you use these apps at high volume.

Frequent refund and balance activity on third-party payment platforms can intersect with IRS Form 1099-K reporting thresholds, so track what’s a genuine refund versus taxable activity throughout the year.

-

Avoid relying on instant refunds for international purchases.

Cross-border transactions typically fall back to standard multi-day processing regardless of the platform’s domestic instant refund marketing, since real-time rails don’t yet interoperate across currencies and countries.

-

Monitor your account balance for a few days after any instant refund, especially on disputed or unusual purchases.

A credit that looks final today can be reversed once a platform’s fraud review catches up, and catching a clawback early prevents a surprise negative balance.

-

Separate personal and business refund activity if you run a side business.

Instant refund features are generally built for personal-account volume and use cases; business accounts handling refunds at scale should verify their platform explicitly supports commercial use before depending on the feature.

Related reading: Deep Dive: The Rise of AI.

Frequently Asked Questions

Are instant refund apps safe to use for large purchases?

They’re generally safe for purchases within the platform’s stated instant cap, like Revolut’s €1,000 threshold, but larger amounts typically trigger additional verification that slows the process anyway. For anything above a few hundred dollars, expect some friction regardless of the app’s marketing.

Why did my instant refund get reversed after it already showed up in my account?

This usually happens when a platform’s fraud review flags the original transaction after the fact, or when a merchant disputes a return following inspection of the returned item. The credit isn’t truly final until the dispute window closes, which can be days or weeks after the money first appears.

Do instant refund apps charge fees for standard transfers too?

Most major platforms, including PayPal, Cash App, and Revolut, offer a standard transfer to your bank account for free, charging a fee only for the instant or expedited option. Check your specific app’s fee schedule, since these percentages and flat fees change periodically.

What happens if I don’t ship a returned item back in time after using a service like Refundid or Reshop?

These services typically charge your original payment method for the refunded amount if the item isn’t shipped back within the promised window, often seven to fourteen days. Read the specific terms for your chosen service before relying on the advance refund.

Can a fintech app legally withhold a refund past a promised timeframe?

Regulators have taken action against companies for doing exactly this. A 2024 CFPB enforcement case resulted in $4.6 million in fines and redress against a fintech firm for allegedly withholding account-closure refunds beyond a promised 14-day window, showing this kind of delay can carry real regulatory consequences.

Is it worth paying for an instant transfer instead of waiting for a free standard one?

Usually not, unless you have an immediate, specific need for the cash. The fee for speed is often far larger than the interest you’d lose by waiting a few days, as shown in the worked example throughout this guide.

Do international purchases qualify for instant refunds?

Rarely on the same timeline as domestic purchases. Cross-border transactions generally fall back to standard multi-day processing because real-time payment rails like FedNow, RTP, and SEPA Instant don’t yet interoperate across currencies and countries.

Sources

- Consumer Financial Protection Bureau, CFPB Orders Operator of Cash App to Pay $175 Million and Fix Its Failures on Fraud

- Federal Reserve, Pay by Bank and the Merchant Payments Use Case Benefits

- Hudson Cook, CFPB Takes Action Against Fintech Company for Alleged Withholding of Consumer Refunds

- Consumer Financial Protection Bureau, Official Site

- Federal Reserve, About FedNow Service

- The Clearing House, RTP Network Overview

- Revolut, Legal and Policy Pages

- Cash App, Terms of Service

- Internal Revenue Service, Understanding Your Form 1099-K